How to enjoy our new magazine:

Just scroll!

Click or tap the table of contents icon in the menu bar to find any article.

Read any article by clicking or tapping the read full article button below each article intro.

Jump back to your previous browsing spot from any article using the menu bar or back to issue button.

**Incident data obtained through Storelocal® Protection.

†Application data was retrieved from the Apple App Store.

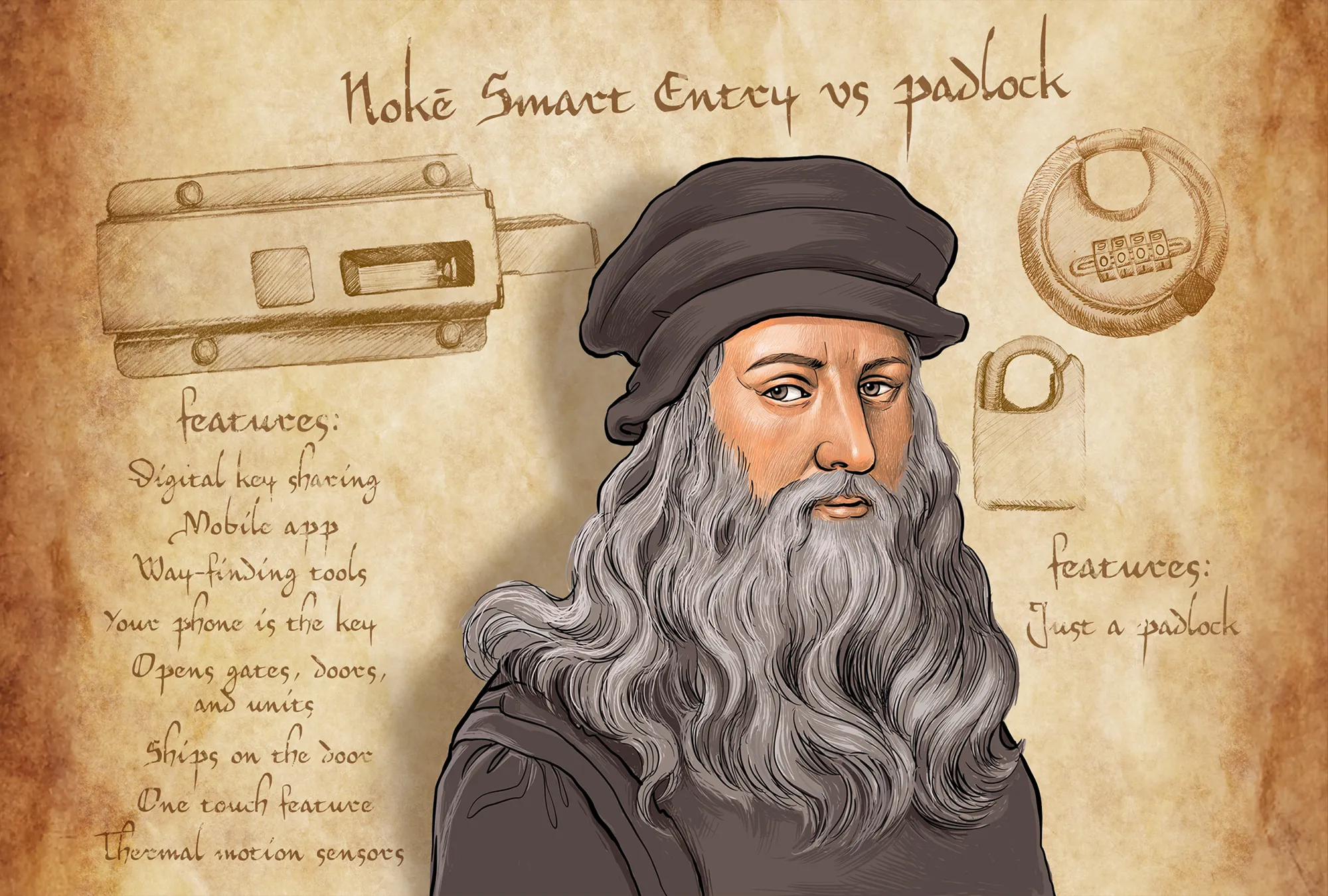

from Janus International. Along with Janus, Nokē and R3 help to enhance both the owner

and customer experience and boost your bottom line.

For over 20 years, Janus International has led the way with turn-key self-storage building solutions, from premium roll-up and swing doors to state of the art security technology and facility automation tools.

-

Embracing Technological TransformationPage 14

-

Five Steps To Turn Negative Thoughts Into Positive ActionsPage 18

-

Refining Your Operational StrategyPage 20

-

The Right To Increase Rental Rates In Self-StoragePage 22

-

The Next Generation Facility Depends On VideoPage 24

-

How To Outrank Your CompetitionPage 26

-

The Benefits Of Insulated Metal Panels In Self-Storage ConstructionPage 73

-

The Right Layout And Unit Mix For Your FacilityPage 78

-

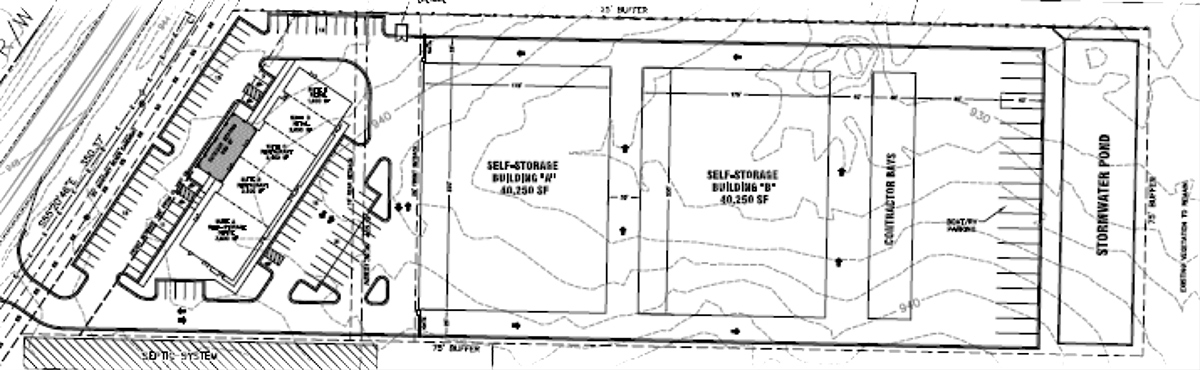

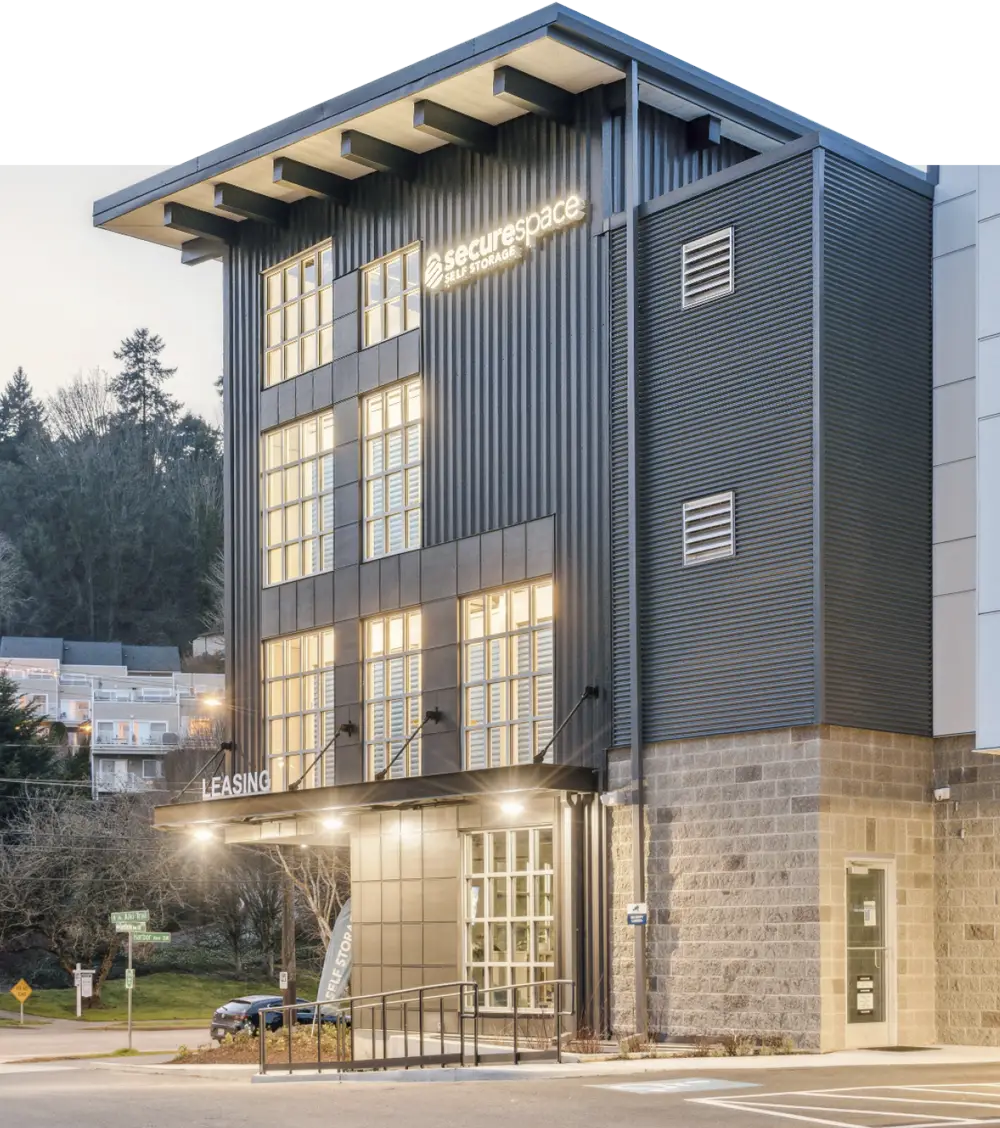

Harbor Avenue Self Storage in Seattle, Wash.Page 82

-

Overcoming The High Cost Of FundingPage 86

-

The 12 Lessons Of 2023Page 90

-

Cracking The Code Of Site SelectionPage 92

-

Rate Expectations For 2024Page 94

- Chief Executive Opinion by Travis Morrow 6

- Publisher’s Letter by Poppy Behrens 9

- Meet The Team 10

- Women In Self-Storage: Sue Haviland by Erica Shatzer 31

- Who’s Who In Self-Storage: R. Christian Sonne by Erica Shatzer 35

- StorageGives 101

- Self Storage Association Update 103

- The Last Word: Kelly Gallacher 104

For the latest industry news, visit our new website, ModernStorageMedia.com.

hat is a storage facility? This is always a tricky definition when trying to count stores. I’d say you’re still in the industry with 100 units, maybe just getting your feet wet, but anything less than 200 units (maybe 250?) and you don’t have a commercial-grade storage facility.

He’s also the president of National Self Storage.

-

PUBLISHER

Poppy Behrens

-

Creative Director

Jim Nissen

-

Director Of Sales & Marketing

Lauri Longstrom-Henderson

(800) 824-6864 -

Circulation & Marketing Coordinator

Carlos “Los” Padilla

(800) 352-4636 -

Editor

Erica Shatzer

-

Web Manager / News Writer

Brad Hadfield

-

Storelocal® Media Corporation

Travis M. Morrow, CEO

-

MODERN STORAGE MEDIA

Jeffry Pettingill, Creative Director

-

Websites

-

Visit Messenger Online!

Visit our Self-Storage Resource Center online at

www.ModernStorageMedia.com

where you can research archived articles, sign up for a subscription, submit a change of address.

- All correspondence and inquiries should be addressed to:

Modern Storage Media

PO Box 608

Wittmann, AZ 85361-9997

Phone: (800) 352-4636

theparhamgroup.com

We Listened!

or more than 43 years, Messenger magazine has been the leading authority in the self-storage industry, providing the most comprehensive data, analysis, and expert insights in its monthly issues. Over the years we have had numerous requests for archived articles from our issue library. Finally! The archived editions are here!

We are proud to announce that MSM has unlocked our vault of archives! We now offer more than 43 years’ worth of self-storage articles for FREE! By visiting our website at www.modernstoragemedia.com, readers now have access to more than 40,000 pages of storage-specific content reaching all the way back to 1979. Searchable by keyword, you will find all our past content, which can be downloaded as high-resolution PDF files.

We invite you to visit our website and explore the past trends and issues of the self-storage industry in a format that simplifies the search process. Explore everything from trends, news of the past, and industry data right from your desktop, tablet, or phone.

You asked! We listened! Now it’s time to enjoy a walk down memory lane to find the information you need! For more details about how you can browse our archives, see here.

Publisher

We Listened!

or more than 43 years, Messenger magazine has been the leading authority in the self-storage industry, providing the most comprehensive data, analysis, and expert insights in its monthly issues. Over the years we have had numerous requests for archived articles from our issue library. Finally! The archived editions are here!

We are proud to announce that MSM has unlocked our vault of archives! We now offer more than 43 years’ worth of self-storage articles for FREE! By visiting our website at www.modernstoragemedia.com, readers now have access to more than 40,000 pages of storage-specific content reaching all the way back to 1979. Searchable by keyword, you will find all our past content, which can be downloaded as high-resolution PDF files.

You asked! We listened! Now it’s time to enjoy a walk down memory lane to find the information you need! For more details about how you can browse our archives, see here.

Publisher

We have put every issue through 2022 on our website, giving you free access to this wealth of knowledge.

- Year or Topic

- Person or Facility

- Market or Company

This free archive is a powerful tool you can use to see how far the industry has come and to discover how the past helped shape our future.

Modern Storage Media

Messenger

eople have always feared change. This fear is deeply ingrained in us, even though we are often taught from a young age that change is the only constant in life. Many sectors feel this fear. They have long had traditional practices. One such sector where this fear is notably prominent is the self-storage industry.

Traditionally, for a vast majority of self-storage operators, the incorporation of technology was limited to the bare essentials. These typically included an electric gate for security, a digital sign for marketing, and a basic personal computer in the office. This computer often ran rudimentary property management software, in many cases, simply a spreadsheet program like Microsoft Excel. Historically, the self-storage industry did not heavily rely on advanced technology as a means to enhance various aspects of business operations. There was little focus on using technology to increase revenue. It also wasn’t used to improve the efficiency of lead acquisition and rental processes or streamline operations during move-out or transfer.

However, the landscape began to shift dramatically in the post-COVID era. Today, the reliance on technology has become not just a matter of convenience but a necessity for the continual improvement of revenue generation and occupancy rates in self-storage facilities. Contemporary property management systems now play a pivotal role. These systems have the capability to identify and highlight best-selling units. This information is crucial and can be strategically utilized to adjust pricing and promote these units on various acquisition channels. Modern technologies empower self-storage operators to influence consumer decisions through sophisticated website design and online marketing strategies. They enable customers the convenience of renting a unit online at any time, say at 9 p.m., while in their pajamas, and moving in before the office opens the next day. This process is facilitated by advanced electronic doors and gates that interact with software to provide tenants with necessary access codes upon completion of the online rental process.

The challenge then becomes: How do we, as an industry, overcome our ingrained fear of change? The answer lies in recognizing and embracing the advantages that technology brings. Operators see how technology makes their businesses efficient and effective. It allows seamless 24/7 operations, so they start to integrate these new systems and processes into their operations. This infusion of technology, while beneficial, is not without its challenges. It brings a mix of positive and negative outcomes, and it demands a prudent, logical approach when beginning the journey of technological integration.

Technology has had a big positive impact in our industry. It has made data, solutions, and oversight widely available for our facilities and businesses. Data gives us power. It lets us understand and use market trends, seasonal changes, economic impacts, and competition. We can do this in a new and dynamic way. The idea of reverting to old methods becomes unimaginable once we experience the benefits of these advanced systems. Another notable advancement is the possibility of extending operational hours. The concept of a self-storage facility operating 24/7 was unheard of several years ago, but it’s now a feasible reality thanks to technological advancements.

However, the adoption of technology is not without potential pitfalls. Firstly, the cost of implementing cutting-edge technology can be significant. Additionally, not all technological systems are designed to integrate seamlessly with one another. Operators must find systems that align well. These systems ensure that investments yield benefits. They should not complicate or hinder the operation. Another risk is becoming too reliant on technology. This can make us neglect the need for ongoing personal and professional growth. Understanding and interpreting data trends is helpful, but it’s equally important to keep making business decisions based on experience and industry expertise. This is especially true when data may not provide clear guidance.

In terms of operational efficiency, technology has the potential to revolutionize every facet of daily operations in a storage facility. Cloud-based property management software, for instance, has improved various operational aspects. We now follow up with new tenants in real time. We tailor follow-ups to their needs and timing. We also see right away which inventory is vacant and ready for move-in. The move-in and move-out processes were managed by an on-site manager. They used extensive paperwork, printers, and filing, but the processes have been streamlined. Modern technology enables prospective tenants to check unit availability and pricing online. Coupled with electronic gates and doors, tenants can now move in without the need for direct interaction with a manager. Similarly, the move-out process has been simplified. Tenants can indicate their intention to vacate online, upload photos of the now-empty unit, and have these documents automatically appended to their tenant profiles. This makes the process smoother. It also helps customers. It makes them more likely to come back for storage.

Security is another critical aspect that has been enhanced through technology. Modern surveillance cameras now have artificial intelligence. They can recognize individuals and read license plates. This tech advance adds security. It speeds reviews during incidents. It aids in assessing and preventing damage.

In the realm of competitive advantage, technology is leading the way. These systems offer insights into competitor pricing. They recommend pricing strategies based on market analytics. They also provide valuable demand indicators for various unit types. These systems also inform rent raise strategies. They bring data-driven insights that enable better decisions about fee changes.

The second strategy involves careful and measured implementation. Rather than trying to overhaul all systems at once, a phased approach is better. It starts with non-critical areas and allows for a smoother transition. This method allows for adjustments and feedback. It ensures that the changes are indeed helping the facilities.

The third strategy involves collaborating with tech companies. They specialize in self-storage. Customizing technology solutions to fit specific needs is crucial. These companies can offer expert guidance. They will instill confidence. The changes will help operations, customers, and our market.

Change can be daunting, especially in technology, but embracing it is vital for the growth and future success of the self-storage industry. As tenants continue to integrate technology into their personal lives, it is imperative for the industry to evolve in parallel. This approach ensures competition. It also fosters innovation and long-term success. The world is increasingly driven by technology.

o you have a Negative Nancy or Toxic Tim whom you’re keeping longer than you should? Would you let them go if you weren’t so short staffed? One Negative Nancy or Toxic Tim infiltrates the whole company and it spreads throughout, affecting everyone.

Think of it like this: You attend a meeting that Negative Nancy was in. When you leave, you approach Positive Polly and share with her, “It’s so frustrating dealing with Negative Nancy. Why is she still here? All we do is constantly listen to her babble about her unhappiness.”

Before you know it, you become a Negative Nancy, and Positive Polly sees the impact the original Negative Nancy has made on you and the team. It only takes one person thinking negatively to bring the whole environment, culture, and team down. In order to help you, Positive Polly shares the following:

You have 60,000 thoughts a day, and 80 percent of them are negative. These come in the form of doubt, worry, and stress and are linked to poor attitudes, declining engagement, and poor performance.

Most people think they are positive and optimistic, yet negativity shows and they don’t recognize it. In fact, 95 percent of your thoughts are repetitive. So, all of the negative thoughts keep getting repeated, impacting how you show up, speak out, lead, and live.

Your thoughts are the fundamental foundation of everything you do and everything you don’t do, yet oftentimes you don’t think about them. When was the last time you thought about what you thought about?

If you’re like most people, you think the same way you’ve always thought, resulting in the same behaviors, actions, and results. If you want to change relationships, communication, interactions, your confidence, you must first change how you think. Once you change that, then everything else will change as well.

Here is a five-step process to help you change your thoughts to invoke different actions, behaviors, and results and develop a positive work environment.

The more you work through this process, the more positive thoughts you have. You’ll soon recognize negative thoughts in others and can help them master their own mindset. You’ll become the Positive Polly and help develop a positive work environment that no one wants to leave.

ar too often, there is a lot of hope in operating self-storage sites. Hoping that the lease-up will go well. Hoping that the rates will be strong; and of course, hoping that you have the right team in place. You can get mad, anxious, or even pray through this process, but simply hoping for good won’t take you far.

After running and operating storage sites for over a decade, I’ve learned that operations require more planning and adaptation than most people realize. The best thought-out plan will change. The people or staff can change, and even market conditions will change. The real separator is your resourcefulness to adapt to these changes.

The advantage we have as small operators is the ability to focus on the things we can change or adjust, but we can also act quickly. Unlike giant organizations, our companies and teams are like a sports car weaving through the mountains rather than a tractor-trailer at a steady and certain pace. So, your resourcefulness as an owner, operator, or even a manager can be the most significant difference in the success of your operations.

As Jeff Bezos from Amazon has famously said, “Be stubborn about the vision but flexible about the details.”

This principle should be the cornerstone of our strategy, guiding us to embrace change with confidence and agility.

As a multi-site operator, it’s essential to manage the big picture and assess the whole portfolio first and then each individual site as it substantially impacts the collective group. If a basketball team is the collection of the players, then our sites are the collection of our portfolio. However, unlike a basketball team with some players on the bench and on some on the court, all our players are active all the time, and their contributions can either pull us up or down.

There are many ways to look at this, but like your GPA in school, adding As to your scores will most definitely make an impact. So, once you’ve zoomed out to see the big picture, it’s time to zoom back in on each and every store. To do this, we’ll start with the past of the PPF (past, present, future) method.

Today, my view is vastly different. The past is an incredible teacher, and learning from it can protect and propel you into a better future. So, when it comes to evaluating storage sites, I start here.

To do this, I take the time to really study the site. How have things been going? What has happened with the key stats of the site over the last few months or even years? How has the management team performed? Have we hit any goals, or were they even set in the past?

Understanding the past is the first step and will set you up for the next step: the present.

To learn from the present, ask questions like: How is the site doing today? What is working well? What needs to be fixed? Are there areas of concern or goals that need to be established?

Critical questions like these help determine your site’s current state and prepare you for what’s to come. This also is the opportune time to create goals, add structure, and redefine your current strategies.

Evaluating the current situation is critical and worth the investment, so don’t dismiss the value of help.

Whether you bring in an experienced consultant or even simply friends and family to check out your sites, it’s ideal to bring fresh eyes to your business. Let others experience your site, and ask them to share the good, the bad, and even the ugly. Embrace the feedback, and don’t feel it as criticism but as an opportunity to improve.

From here, it’s time to accept where you are, understand your new goals, and plan for what’s ahead: the future.

In self-storage operations, I’ve determined that the only way to look at the future of our storage sites is with optimism. Some won’t agree, but the mission of bringing a positive and engaging strategy to your operations will take you extremely far.

The truth is, there is always something to improve, and you must find it. If you don’t, keep looking, hold your head up, and keep going until you see the opportunities. Progress is greater than perfection; even small steps can build momentum to improve your success.

To ensure you’re not just dreaming about a brighter future but actively moving towards it, set tangible, measurable goals and follow a roadmap into the future. Whether boosting occupancy rates or improving customer satisfaction scores, having real targets provides direction and motivation for the team. Without these, you’ll be left to the rhythms of life and back to just hoping for good.

For each of the above, follow the pattern of the PPF method and ask key questions.

Sales

- Past: How have sales trends evolved in the past? What strategies yielded the best results?

- Present: What is the current performance like? Are we meeting our targets? Are they set?

- Future: What new sales strategies or opportunities can we explore? How can we innovate our sales approach to stay ahead?

Marketing

- Past: Which marketing campaigns were most effective? What can we learn from the feedback?

- Present: How are our current marketing efforts performing? Are we engaging our target audience effectively?

- Future: What emerging marketing trends should we adopt? How can we better align our marketing with customer needs?

Team

- Past: What strengths and weaknesses have we identified in our team dynamics?

- Present: How is the team performing? Are there any immediate areas for improvement or training needs?

- Future: How can we foster a culture of continuous improvement and professional development?

Quality Assurance

- Past: What have been our significant quality challenges, and how have we addressed them?

- Present: What is the current state of our quality assurance practices? Are we on a routine?

- Future: How can we raise the bar for quality and customer satisfaction? What would excellence look like?

Customer Service

- Past: What feedback have customers provided about their service experience?

- Present: How are we currently measuring up to customer expectations? Does our customer base think highly of us?

- Future: What innovative customer service strategies can we implement to enhance customer loyalty and satisfaction? What does winning in customer service look like?

In weaving these considerations throughout our operations, the PPF method becomes a strategy and a mindset guiding us toward excellence in a simple and accessible format.

Ultimately, hope is not a winning strategy. The diligent application of the PPF method will lead you to operational excellence and success. By learning from yesterday, taking action today, and planning for tomorrow, we will empower ourselves to achieve our goals and fulfill our vision for the future.

elf-storage rental agreements, as written, are month-to-month leases, subject to renewal. But built into these short-term occupancy agreements is the contractual right of the owner or landlord to increase the rental rate by giving the customer or occupant advance notice of the change. Pursuant to that change notice, the occupant is given the right to vacate prior to the effective date of the new rental rate, thereby avoiding the rental rate increase. If the occupant elects to stay on the premises, they consent to accepting the published higher rate. At least until the next rate increase comes down the pike.

This risk of rate increases is highlighted by the “CHANGES” clause of a month-to-month rental agreement which contains a clear notice to the occupant that their rental rate is subject to change after thirty (30) days’ notice. Remember again, these leases are month to month, not just for the benefit of the owner, but primarily for the occupant, who may consider their storage needs as only short term. A year-long lease, albeit one that would secure their rate for a longer period, limits a user’s flexibility to vacate when their short-term storage use is no longer needed. But that month-to-month flexibility creates a business opportunity for self-storage owners. Oftentimes, occupants end up needing their storage units for longer than they anticipated, which, by agreement, allows the owner to change the rental rates. Occupants who accept the advantages of a short-term occupancy subject themselves to the risk of periodic rate increases.

A typical “Changes” provision reads as follows:

CHANGES: All items of this Agreement, including but without limitation, the monthly rental rate, conditions of occupancy and other fees and charges, are subject to change at the option of the Operator upon thirty (30) days’ prior written notice to the Occupant. If so changed the Occupant may terminate this Agreement on the effective date of such change by giving the Operator ten (10) days’ prior written notice of termination after receiving notice of the change. If the Occupant does not give such notice of termination, the change shall become effective on the date stated in the Operator’s notice and shall thereafter apply to the occupancy hereunder, whether or not Occupant has agreed to the change in writing.

These rent adjustments are more likely to occur when an occupant initially leases their storage unit subject to a discounted rate, or under a “concession” agreement, where the owner accepts a move-in at a discounted rate for a finite time, after which the rental rate will revert to the standard “street rate” for the rental unit.

If facilities are offering discounted or concession deals to increase rentals, it is important that the prospective customer be provided with the clear terms for that deal, most notably the time period when the discount ends and the revised rental rate begins, as well as the fact that the revised rental rate itself is subject to change over time. In the case of short-term rentals, a customer must be prepared to accept that, in exchange for the ability to terminate and vacate whenever they want, should they choose to stay on the premises, they must pay the rate as offered by the owner.

All this talk of increasing rental rates and fluctuating prices has legislatures around the country considering the possible need for rent control in self-storage. Proposed legislation in Texas and New York all failed to move forward, likely due to the reality that self-storage pricing is simply a matter of choice and contract. Every prospective and current tenant is free to leave if they don’t like the price of their rental unit. The market dictates the price. It’s as simple as that. If the tenant chooses to stay and use the premises, they are obligated to pay the rent that is being charged. Self-storage is not a necessity. It is a discretionary purchase. Storing personal property in a rented space is a voluntary decision by a customer. Again, if they don’t like the price offered by their landlord, they can vacate and move to another location.

While there is certainly no illegality in offering discounted rates to incentivize customers to rent, these concession agreements, often phrased as “dollar move-in” specials, are often fraught with complications for businesses that do not clearly communicate the terms and conditions of these deals to their customers. The general recommendation is that a customer sign a rent discount addendum with explicit terms and conditions concerning the discounted prices and their eventual change. This type of transparency is an effective solution to resolve all the angst and noise about rent concessions and resulting rent adjustments.

Customers

Depends On Video

ver the past few decades, self-storage has grown into a resilient asset class that has provided a way to diversify commercial real estate portfolios and has proven to perform well through market cycles. In 2021, the global self-storage market was valued at $54 billion and projected to grow annually by 7.53 percent1 between 2022 and 2027 to reach $83.6 billion at the end of 2027. The North American market is projected to contribute the most significant chunk of this figure.

As self-storage owners grow their footprints, more and more are looking for the best ways to run unattended facilities. Many are turning to new tools like live two-way video and the use of video recordings to do so. They aim to reduce operating costs and consistently rent more units while maintaining or growing customer satisfaction.

Here are six things that two-way and recorded video technology can support for facility owners and operators in 2024:

In addition to searching for a facility online, potential new tenants visit facilities when looking for an option locally. Some owners struggle with missing a potential customer due to the main office being busy or team members not being available. You can also use live video as a simple and effective way to capture in-person leads. By posting a QR code in the main office that, upon scanning, starts a live video call with a representative, potential tenants can get in touch with a team member immediately. The same QR code can be placed around the facility on the side of the building, in the main office, and on gates to capture leads actively.

As consumers expect faster response times and touchless ways to rent a unit, unattended storage facilities are growing in popularity. Ideally, they help lead to compounded growth and the opportunity to remove owners and operators from regular operations, open additional facilities, or both. New technology is accelerating the adoption of the unattended facility model and the ease of introducing it to owners and customers.

ike it or not, when it comes to marketing, you are always competing with someone for your target market’s business. You may be blessed to have little or no direct competition, but what else are you competing against? Alternatively, you may be in a highly competitive area with your main competitor right across the street. At any rate, you still need to stand out above the crowd. There are various ways to do that in today’s digital marketing age, so I’ll highlight some examples of clients of mine with low, medium, and high competition.

If your website has been up for a while, where do you come up when someone searches for your main keywords or phrases? Your goal is to improve that position by bumping your competition down and putting yourself above them in the search results. Keep in mind that Google brings up the freshest, most relevant, and most useful content that matches the searcher’s query. If your website is brand new, you have some work to do.

First, I’ll tell you about one of my clients who opened the very first Rage Room in Tempe (and the whole state of Arizona). Being the original, he had no competition. He enjoyed being on the first page of Google search for “rage room Phoenix” and “anger room Tempe,” among other phrases. Even if the searcher didn’t know the name of the company, he was found by searching for what it is. That’s one of the first things to remember when it comes to search engine optimization: What is your target market going to enter into the search box to find what you are offering if they don’t know your name?

For almost two years my client enjoyed being the only one in the Phoenix Valley until another rage room opened nearby. At a networking event, I met someone who opened one in the North Valley. My client can’t afford to become complacent; he has to continue his marketing efforts or he’s going to lose the coveted top spot on Google.

He told me he liked working with older people, helping them with “healthy aging.” That gave me the idea for him to offer a “healthy aging screening” that would get folks into the office. Then, depending on their medical problem, he could offer various treatments. That helped him stand out and reach a specific target. We focused on sharing articles on healthy aging, and we built a following with that strategy.

- Find out how often they blog. With the free e-news reader Feedly.com, you can subscribe to their blogs without them knowing or having to receive their emails.

- Create a “private list” on X (formerly Twitter) and pin it to the top of your X app to monitor it. You can see how often they post and what they are posting. Copy (or improve upon) some of their ideas!

- From your LinkedIn Business Page, you can follow your competitors’ business pages. Go to Analytics in the left menu, then to the Competitors tab. Go to “Edit competitors” and search for your competition. If they don’t have a LinkedIn Business Page, then you’re ahead of them right there!

Now, you’re not just competing against your business competition. You’re up against everyone else that your target follows online and on social media, which includes but is not limited to:

- family

- friends

- celebrities

- entertainment

- major brands

- politics

- the latest news or trends

So, what’s an independent self-storage owner supposed to do?

- First and foremost, clearly define your target market personas. You can have more than one. The free workbook at https://azsocialmediawiz.com/define-target-market-workbook/ is a good starting point.

- Determine what sets you apart from the rest. What makes you different? What makes you unique? What’s your unique selling proposition (USP)?

- Research the target(s). Get to know them. Which social media networks do they frequent the most? Do generations factor in? What are their pain points? What are their other interests? (That’s what you’ll be competing with for their attention online.)

- What keywords are they going to enter into the search engine to find you? Use Google’s free keyword tool (https://ads.google.com/home/tools/keyword-planner/). The keyword list will tell you which phrases are most searched for each month. It will also give you variations of keywords and phrases. You can get a list by location and try several different phrases. This list will help you write the copy for your website and social media network profile pages and give you ideas for blog articles.

- Who’s your direct competitor? Using an incognito window, do a Google search for your major keyword phrases and questions. Who comes up on the first page? Start with the top organic (non-paid) listings. Visit their websites.

- If they have a blog, how often are they blogging?

- Are they on social media? (which networks?)

- How many followers do they have?

- How often are they posting?

- What are they posting?

- If they’re not blogging weekly, then you need to blog weekly, if not daily, to bump them down and you up. Obviously, if they’re not active on the social networks, then you need to be. The more active you are, the faster you’ll grab their spot in the search results.

- Set up your website and social media networks optimized for local search. Branding must be consistent throughout.

- Set SMART (specific, measurable, attainable, relevant, time-bound) goals. Based on your competitor research, choose metrics that make sense for you.

- Plan your strategic efforts to get your target market’s attention and meet your goals. If competition is low to medium, then organic (non-paid) marketing should be sufficient until more competitors show up (and they will). Since location is a factor, you may also get away with just doing organic marketing. Local businesses with high competition will have to budget for paid advertising or get very creative and clever.

- Then comes the tactical plan to implement the strategy. How many blog articles or videos will you do a week? How many posts to X, Facebook, Instagram, and/or LinkedIn per day?

- Then, just do it. Yes, it takes time to build a following on social media and even to start getting traffic to your website. Clearly, you must put in more time upfront. Figure it will take at least two to three months (depending on how competitive your market is) to start seeing results.

- Monitor and measure at the end of each month to see what worked and what didn’t work. Plan accordingly for the next month. Check your website analytics as well as your social media insights. Compare the results month to month. Do you see improvements? If you put in the effort, you should.

As you can see, it’s not as simple as putting up a website and doing a few posts or ads on Facebook. It’s complex, but it doesn’t have to be overwhelming if you take it one step at a time.

ccording to McKinsey & Co’s “Women in the Workplace 2023” report, the number of women in C-suite positions has increased from 17 to 28 percent since 2015. The report also states that the representation of women at the vice president and senior vice president levels has improved, with both levels experiencing a five-year increase of four percentage points. While these upticks are positive, the fact that a gender imbalance at the executive level remains in 2024 is disheartening, even for the women who’ve managed to reach those ranks.

Sue Haviland, owner of Haviland Storage Services, a San Diego, Calif.-based company that specializes in offering clients solutions that fit their operational needs, whether its auditing, manager training, market studies, short-term consulting, or full third-party management, knows firsthand that women have “come a long way,” especially in the 35 years since she entered the self-storage industry. Unfortunately, like many female professionals, she endured a fair share of gender biases throughout her career and paid her dues before forging her own path. Despite having to overcome some obstacles, Haviland loves this industry and says she’s a stronger leader and mentor because of the people and experiences she has met during her career.

Besides working as customer service representative at Enterprise Rent-A-Car after attending Northern Michigan University, Haviland has only been employed in the self-storage industry. She left the car rental company in 1989 to manage a self-storage facility in Chicago, and she’s been a self-described “storage nerd” ever since.

“I cut my teeth at Extra Space,” says Haviland, who spent 10 years climbing the company’s corporate ladder one rung at a time. Through hard work and dedication, she first received managerial promotions, from site manager to area manager to regional manager, prior to attaining middle management status as the Western regional vice president. Her final title at Extra Space Storage, before leaving the company in 1999, was vice president of operations.

She also saw a need at that time for smaller operators who could benefit from her skill set without needing to have someone in her position on staff full time. She founded Haviland Storage Services in 2009 with the intention of auditing self-storage facilities for fraud on behalf of the properties’ owners and operators. Haviland says starting her own business was “stressful and scary,” but it was also the best move she ever made in her career.

Uncovering theft during facility audits led to new business opportunities. Haviland “fell into management contracts” when several owner-operators, pleased with her audit findings, asked her to manage their properties. Referrals and word-of-mouth marketing generated more business and enabled her company to grow. Haviland, who loves speaking at various industry-related conferences and all the storage friends she has made over the years, has also acquired clients from speaking at conferences.

“For years I never did my own website,” says Haviland, who finds it difficult to tout her strengths. “I always made sure all my clients were covered, but I didn’t promote myself.”

Haviland Storage Services currently has 28 employees and manages 10 facilities—many of which are long-time clients. “I still visit the sites regularly,” says Haviland, “even though I’m no longer a daily ‘road warrior.’ I have team members to do that now. It was hard for me to give that up, but I’m proud of my team and know it’s time to have help and not try to be a one-woman show. It is such a fantastic feeling to know I can trust my teams to help us grow.”

Although the company is mostly regional, primarily serving the Southern California area, it also has a couple sites in Northern California and manages several remote locations in New Jersey, New York, Arizona, and Texas. “They have boots on the ground folks,” she says, adding that Haviland Storage Services received those remote management contracts via referrals from a software company. “If we can make it work,” Haviland and her team are open to remotely managing locations anywhere in the U.S. “We determine if remote is possible on a site-by-site basis.” If the geographic location isn’t a good fit for the company, “I pass potential clients onto peers,” she says. Haviland loves the fact that they have been able to customize their consulting and management plans to fit their clients needs vs. fitting the client into a “mold.”

Moreover, Haviland has handled a wide array of unfortunate and unusual situations for her clients over the years. From fires, floods, corpses, drugs, and burglaries to a boa constrictor, there is one that still stands out for her. “I never knew there was such a thing as a cat catcher until I had to hire one to get 18 cats out of a resident manager’s apartment walls,” she says. “That apartment scene is one you don’t forget.”

In addition to the 10 facilities with on-site management, Haviland Storage Services will be adding two new builds to its portfolio as soon as they are fully constructed. Haviland enjoys the challenge of a new lease-up property or taking an older, mismanaged site and making it shine for her client. She also loves taking on short-term clients and helping those new owners learn how to run their new sites within three to six months.

“Many of the properties in the portfolio are large, thus helping Haviland Storage Services make the Top 100 Operators list for several years,” she adds. “We may only have a few sites, but we have a lot of square footage.”

And Haviland has been using her voice to benefit other women. Last year she was one of the six panelists on the WISE (women in storage education) discussion at ISS’s spring conference—an event attended by more than 140 women who were eager to share their experiences with inequality in the workforce and how they overcame gender discrimination. Haviland will serve as moderator for WISE’s follow-up conference this year.

Speaking of inequalities, Haviland acknowledges that she had been passed over for pay increases and promotions. “You don’t always get credit for the work you do,” she says about being a female professional, adding that being berated, bullied, and treated unfairly was not uncommon. “But challenges make you stronger,” and Haviland is grateful for how her experiences shaped her both personally and professionally.

One unnerving challenge that made her stronger was getting beat up by an angry female tenant. Haviland was in her early 20s when a tenant wrongfully accused her of having an affair with her husband because he had removed all his property from the unit they were renting. Obviously, she reported the incident, but she also requested that her supervisor be present the day the tenant arranged to return for her stored items. When he didn’t show up to protect her from possible harm, she got a German Shepard to accompany her throughout the property. “That experience made me aware of the world,” says Haviland, who eventually replaced her supervisor. “I liked to joke that I was promoted because I got beat up.”

What’s more, in her early years, Haviland says, “I was often one of few women at trade shows.” And most of the other women attending those events at the time were area managers or assistants who were working up the ladder. One woman Haviland admired and learned from was Nancy Gunning, president of Chesapeake Resources, Inc. “She always had time for me,” Haviland says, adding that Gunning’s success encouraged her to keep climbing.

Even though Haviland was active in the industry’s various groups and had plenty to contribute, she was “often invited to be the secretary and keep notes.” Haviland says, “I’d look around and be the only lady in the room!” Despite being discouraged by being pigeonholed into that subservient role, she took it in stride and “did it for a while to observe, learn, and network.” Ultimately, it became an experience of professional growth for Haviland. “It shaped who I wanted to be,” she says. “I always wanted to help others, but it was hard to say no.”

“I’m training others to do every aspect of management,” Haviland says, pointing out that the training will also enable the company to grow and take on new clients and projects.

However, she’s not quite ready to retire. A new granddaughter, Cleo, keeps her working in California, even though she recently built a second home in South Carolina. Until then, and after that time comes, she’ll continue appreciating the work/life balance she created for herself and her family by playing tennis, attending music cruises, and managing operations in the industry she has long loved.

“This has been a lot of hard work but a good ride,” says Haviland. “I’m glad I went from renting cars to renting storage!”

Throughout her career, Haviland has remained an active participant in the industry’s associations and charities as a means for gaining knowledge and giving back. She has served on the California Self Storage Association’s board of directors. Moreover, Haviland was a member of the Self-Storage Association’s Education Committee for nine years and taught its Certified Self Storage Manager (CSSM) courses.

She also serves on Charity Storage’s board of directors as vice chair. “I’m passionate about giving back,” says Haviland. Each site managed by Haviland Storage Services participates in Charity Storage Auctions and the Round Up for Charity program. She’ll even be at the April ISS Conference Charity Storage Booth to challenge people to a round of Hoops for a Cause.

Thankfully, Haviland and her company’s efforts haven’t gone unnoticed. Haviland Storage Services has received best-of-business awards for “Best Operational Consultant” and “Best Manager Training.”

Erica Shatzer is the editor of Modern Storage Media.

s an avid boater, and a former self-storage facility owner, R. Christian Sonne, CRE, MAI, FRICS, executive vice president and specialty practice co-leader – Self-Storage of Irvine, Calif.-based Newmark, likes to call self-storage a “safe harbor investment.”

Relative to real estate, safe harbor investments are considered low-risk investments because they are generally protected from significant declines in value, which makes them an ideal option for investors who are looking to preserve capital. Based solely on that definition, Sonne’s claim that self-storage is a safe harbor investment is substantiated. However, he points to the sector’s performance history to provide supporting evidence.

Indeed, its recession-resistant nature has attracted many investors to the asset class. And the COVID-19 pandemic only reinforced what The Great Recession revealed to outside investors: Both economic downturns and upturns generate demand for self-storage. During recessions, businesses may need to close or downsize, while individuals may face upheavals with their employment and/or living arrangements. Alternatively, economic growth can prompt people and companies to expand or upgrade. Either way, self-storage is often needed and used temporarily or long term to accommodate their space limitations.

“What a surprise during the pandemic, self-storage demand fundamentally increased as dining rooms became home offices or classrooms,” says Sonne. “While there have been some corrections, demand fundamentally increased as household use changed with so many work-at-home jobs.”

For this reason, self-storage has become one of the most attractive commercial real estate investments. It has also evolved into a core asset class for institutional investors thanks to its unmatched performance and potential for standardization.

As far as returns go, self-storage has been the top performing property type in the Nareit index for three decades with average annual returns of 18.83 percent from 1994 to 2021. What’s more, self-storage’s total returns surpassed 21 percent in 2023, according to Nareit data published in the 2024 Self-Storage Almanac’s Investment Performance by Property Sector and Subsector Table.

To be clear, self-storage has outperformed the office, industrial, retail, residential, diversified, health care, lodging/resorts, mortgage REIT, timber, infrastructure, data centers, and specialty sectors for 30 years. In and of itself, that’s an impressive accomplishment and long reign.

Although some may question whether the industry’s lead will last due to softening rental rates and declining occupancies in 2023 and the beginning of 2024, Sonne buoys his sentiment about the industry with his belief that “2023 was an economic correction, a reversion to the mean.” He also thinks 2024 will be more in line with pre-COVID norms, saying that the industry will be “returning to normal this year and next year.”

Speaking of gathering data from the internet, Sonne discourages investors and operators from looking at websites for rates. The “teaser” rates that are advertised online are “asking rates” not “actual rates,” which means they do not reflect what existing tenants pay for those unit sizes. “What they’re getting is more important than what they are asking,” he says.

For instance, some recent negative press about the REITs’ rock-bottom asking rates failed to take their actual rates into account. According to Sonne, although the REITs had “double-digit declines” in the asking rates they advertised on the internet, their actual rates were “above the rate of inflation.”

To obtain actual rates when conducting feasibility studies and appraisals, setting competitive rates, or determining valuations, Sonne says it’s still necessary to “shop” self-storage properties in person or over the phone. Scraping the internet for rates would only skew your results. Moreover, examing rental rate trends through historical data (in addition to the current rates) is crucial for an accurate depiction of a market’s vitality and profitability.

“To look at it at a specific time is not enough,” he says.

There has been speculation that higher interest rates and the ongoing shortage of affordable housing across the country are responsible for a dip in demand, but he doesn’t think “it’s that linear,” as there are plenty of other variables to consider in addition to whether people are moving. In other words, dislocation or downsizing are only two of the numerous demand drivers (and they don’t all begin with the letter D).

“There are lots of determinants,” says Sonne. A few examples include length of stay, household budgets, popularity of unit size/type, and location. Here are his insights on each of those.

- Length of stay: “Length of stay has increased since COVID,” Sonne says, which is positive for occupancy rates.

- Household budgets: Even though inflation has eroded Americans’ purchasing power, the monthly self-storage rent tends to be a mere 2.5 percent of a customer’s household budget. On this subject, Sonne remarks that most people spend more money on coffee or bar tabs than storage. Nevertheless, operators must be wary of what people are willing to spend each month to rent a unit. “There’s a ceiling,” he adds about increasing rates. “If it’s too much money, they pay attention.”

- Popularity of unit size/type: Your customer base and location should determine the unit mix. For instance, facilities located near apartment buildings may rent more smaller units to apartment dwellers without ample closet space, whereas a facility situated among businesses may rent more larger units to commercial clients that need to store surplus inventory and/or files. “Another example is climate control,” says Sonne. “It has terrific demand in some markets but not all markets.”

- Location: Obviously, demand and other details vary by market. Continuing with the boating comparison, Sonne, who has homes in both California and Florida, states that the Pacific Ocean is rough and cold, but the water of the Gulf Coast is warm and calm. Though often asked which home he prefers, he points out the pros and cons of each instead of choosing. Similarly, one must weigh the advantages and disadvantages of the market in question before making a self-storage investment.

Instead of taking a general or national perspective on demand, Sonne reminds investors to focus on the local trade areas where they are considering developing self-storage. “Two-thirds of customers come from a three-miles radius of the facility,” he says. Therefore, it is imperative to evaluate the supply and demand of a market on a micro level to determine whether the area is undersupplied, oversupplied, or at equilibrium.

Not all data is good data, however, and one must consider the source as well as the sample size, data collection methods, and margin for error before relying on the results. Free sources are readily available on the internet, but Sonne says that the data they present is “not gospel.” Within the self-storage industry, there are several reputable, established data providers that have been employed for countless successful investments.

To get a comprehensive assessment, Sonne looks at “as many [data points] as I can.” Just like watching multiple news channels to take in various angles and assemble a more complete account, he advises investors to do the same before making (or rejecting) an investment. “Before I go on my boat, I check the weather, the condition of my boat, the temperature, if it has been a historically good time to take a vacation, etc., to determine whether it’s safe to take the trip,” he says. Investing in self-storage requires that same level of preparatory diligence. Otherwise, you could end up sailing in rough seas.

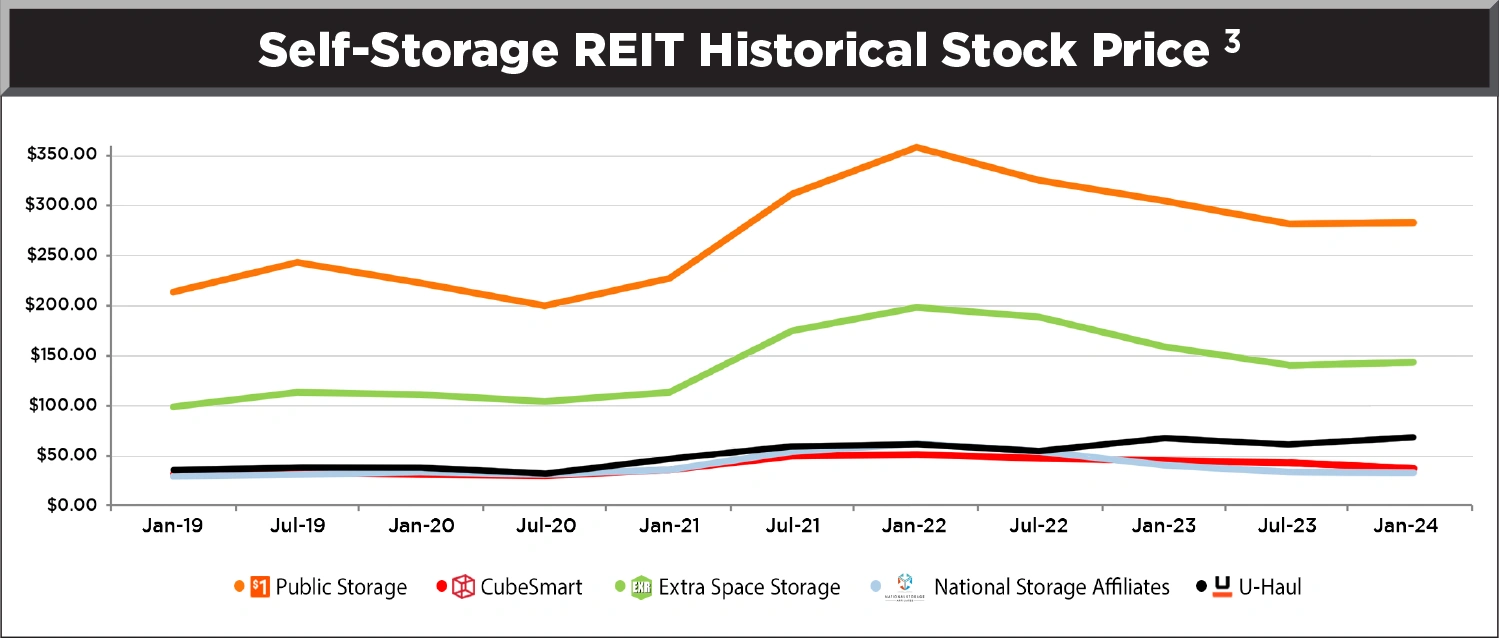

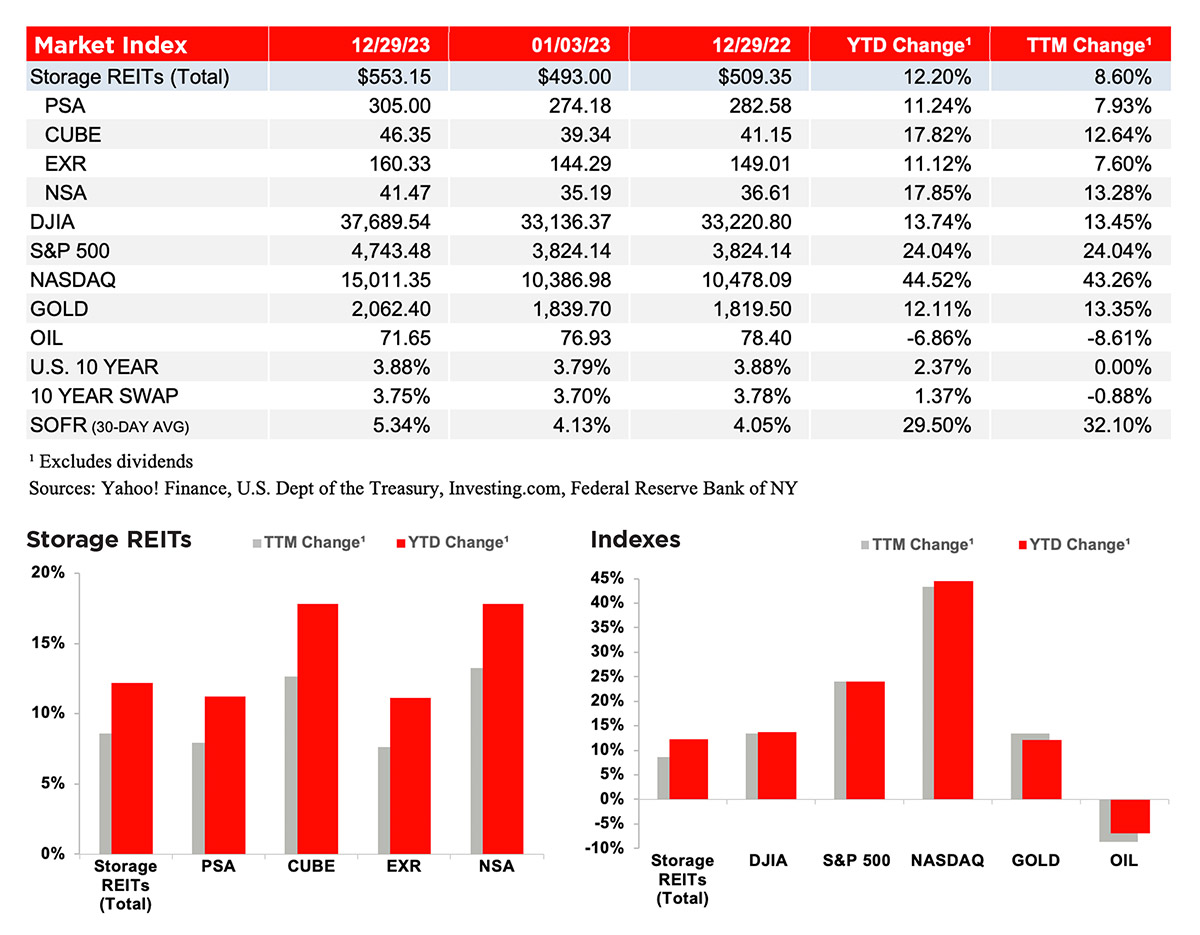

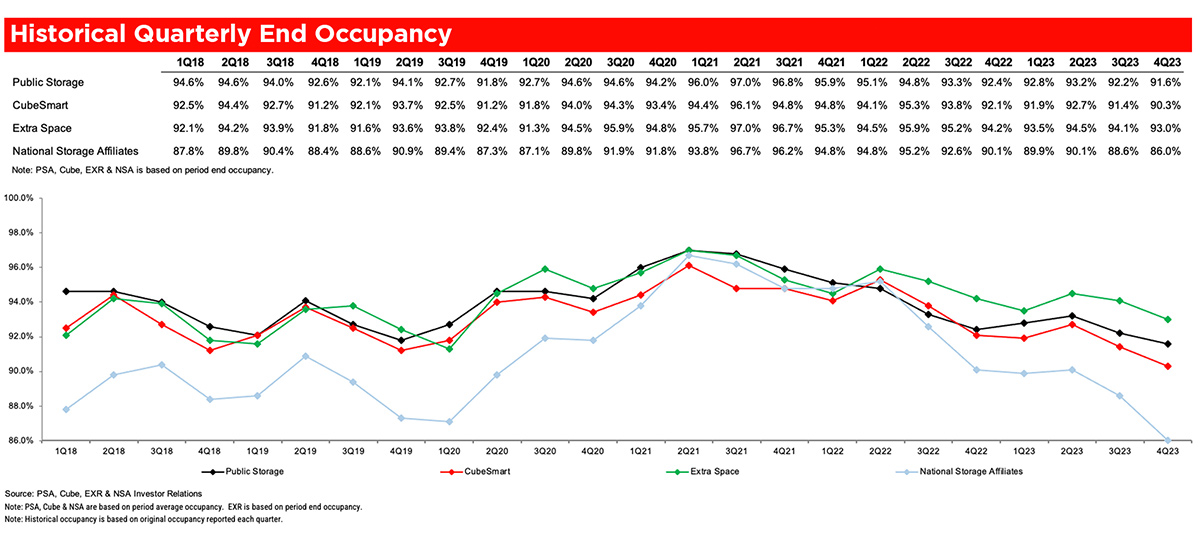

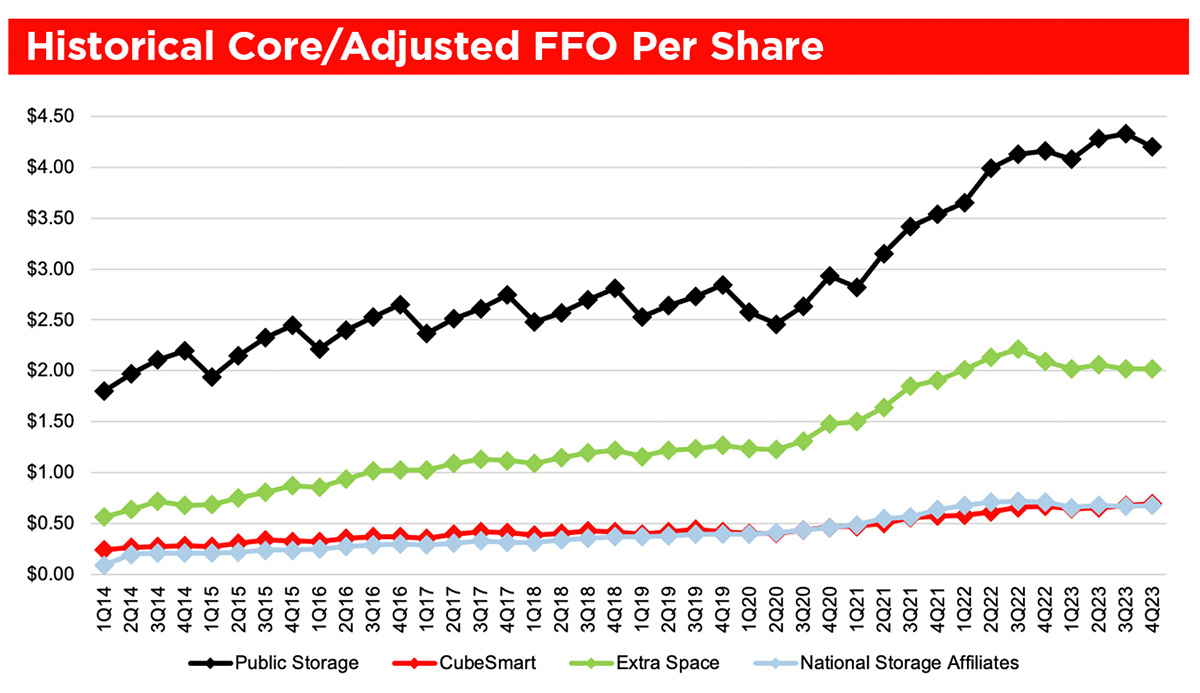

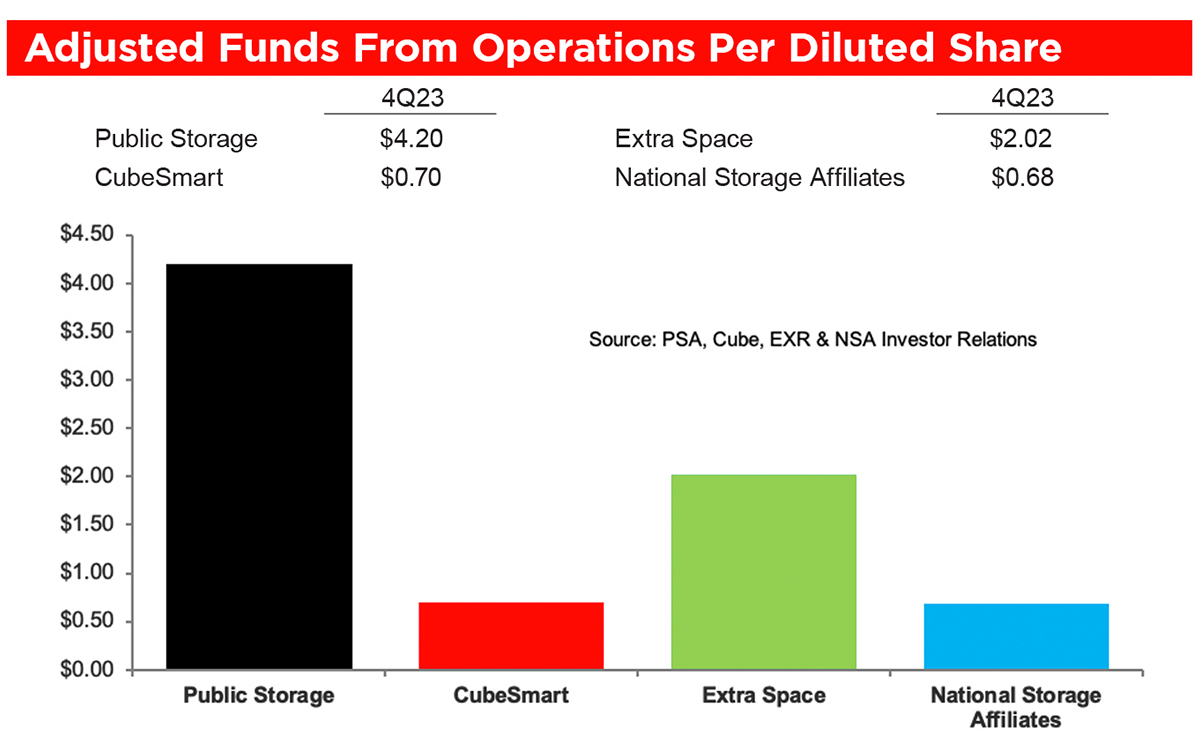

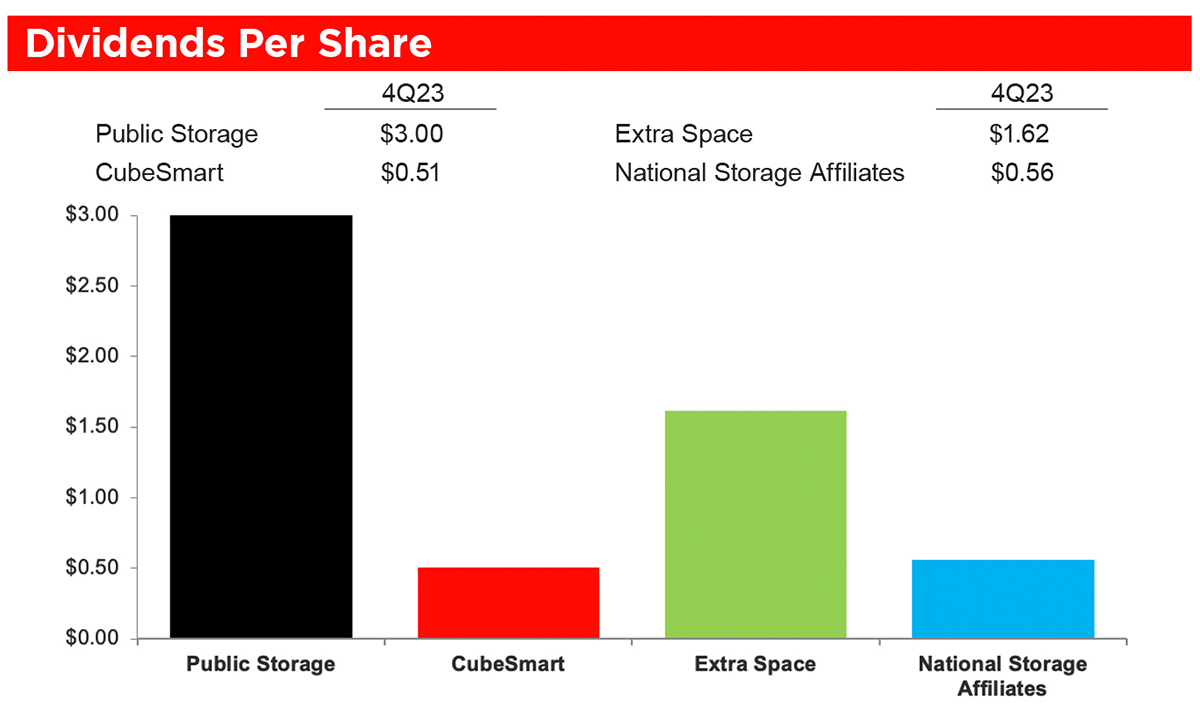

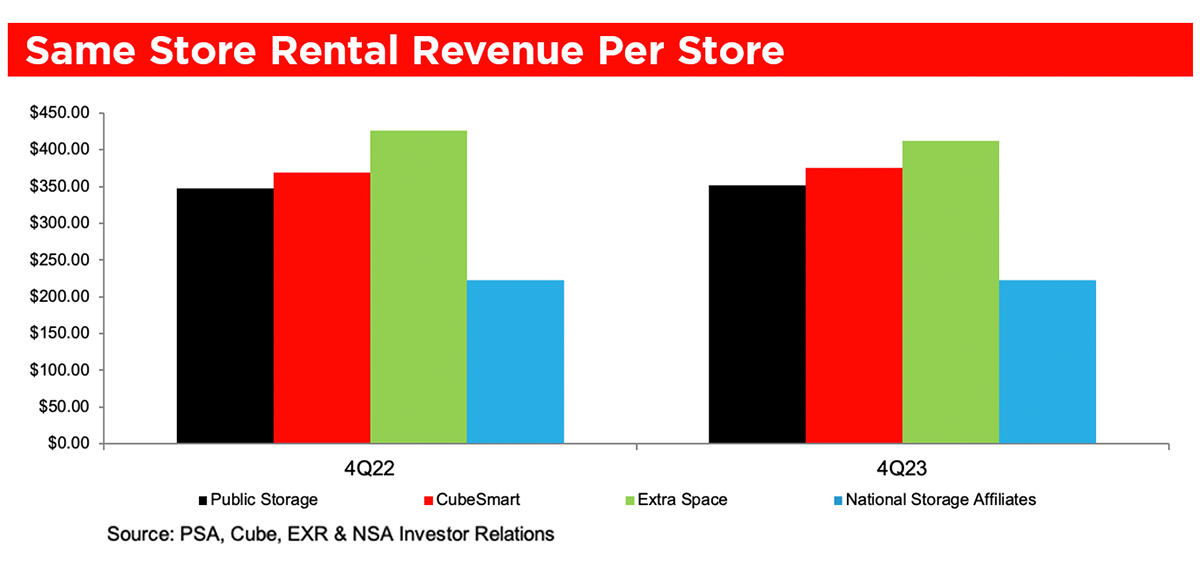

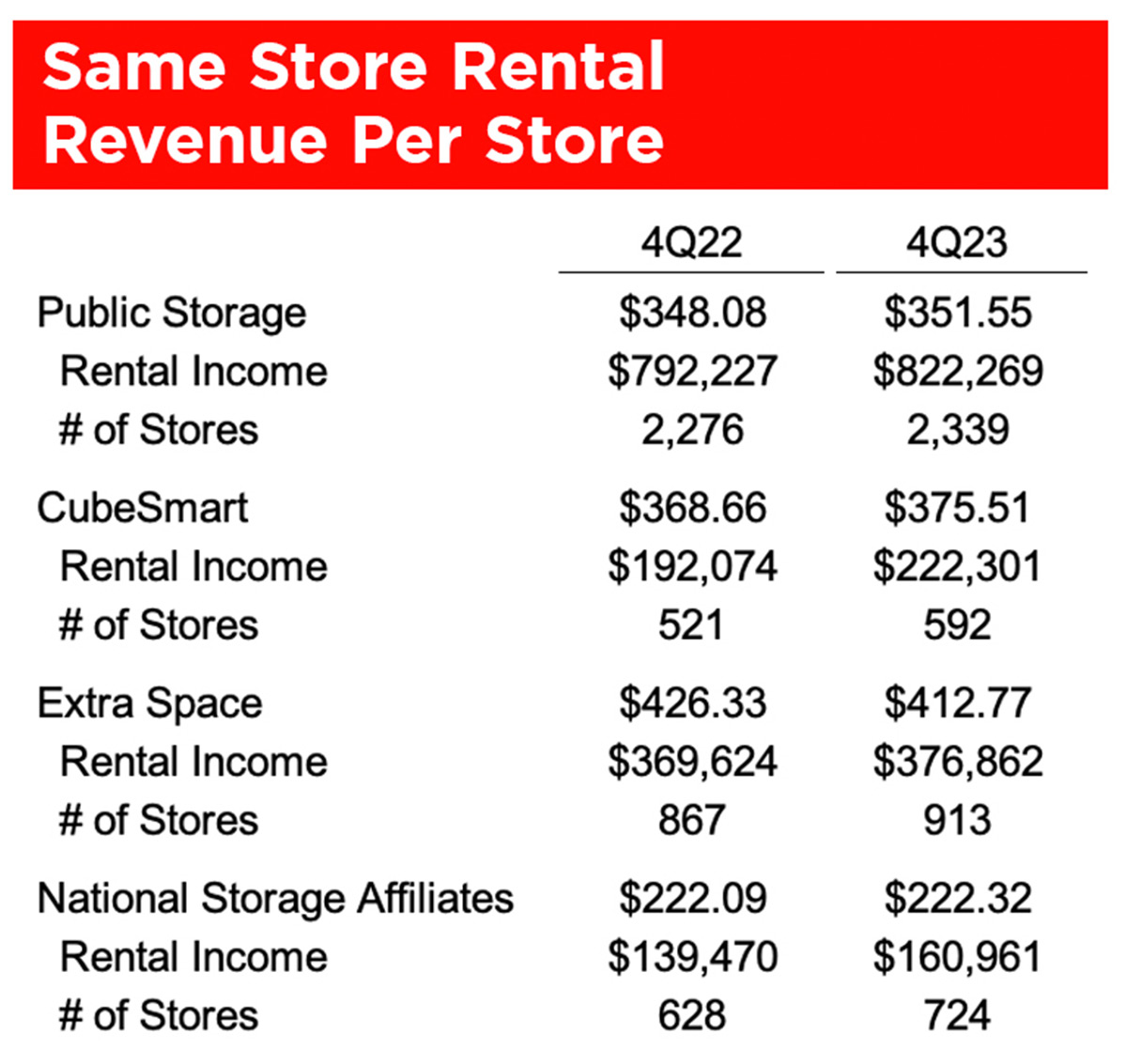

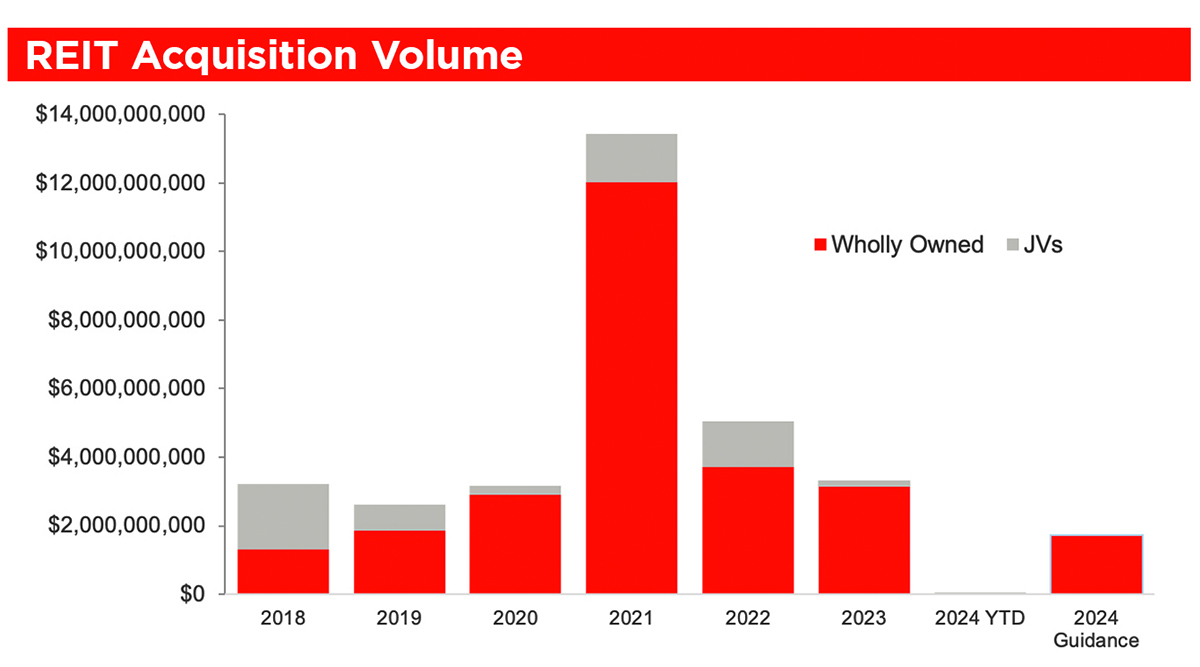

he self-storage sector’s Q4 2023 results and full-year 2024 guidance were in line with expectations. Despite a competitive environment for new customers, the four publicly traded REITs reported positive same-store revenue growth of 0.50 percent (non-weighted) year-over-year in the fourth quarter. Occupancy levels remain strong but have moderated from 2022 to a quarter-end occupancy of 90.2 percent (non-weighted), as the sector returns to a more cyclical operating environment. NOI decreased by 0.25 percent (non-weighted) on a year-over-year basis due to continued upward pressure on non-controllable expenses, including property taxes and property insurance, as well as an increase in marketing spend.

In addition to this quarterly REIT summary, a weekly email from Newmark Group, Inc.’s Self Storage Practice delineates key benchmark rates for the capital markets, near-term expectations for transactions, and interpretive opinions of broader market questions.

The pages of this article summarize the information for the fourth quarter of 2023, reported by the four publicly traded self-storage REITs, along with comparisons between the industry and macro-market benchmarks.

nowing who is renting and what they want is critical to your success as a self-storage operator. Today, millennials rent more self-storage units than any other generation. Born between 1981 and 1996, currently about 28 to 43 years old, millennials comprise 38 percent of renters, according to the SSA’s 2023 Self Storage Demand Study.

A short 10 years ago, self-storage professionals were wondering if millennials would ever rent storage. They seemed to be a generation of vagabonds, who were not getting married or buying homes the way their baby boomer parents did at similar ages.

It seems that millennials are finally becoming their parents. They have steady employment while also starting their own businesses, are making more money, amassing wealth, buying homes, and having babies, like previous generations, even if they took a little longer.

Of course, today’s higher interest rates and sharp appreciation of home prices put a damper on home purchases by millennials and all generations, which is creating pent-up homebuying demand. When interest rates ease, home purchases are likely to rebound, especially among first-time homebuyers in the millennial generation.

Jeff Adler, vice president at Yardi Matrix, started pointing out over five years ago that millennials are a “positive force” for self-storage demand.

Confusing or not, it does chart a course for your response. First and foremost, focus on that age-old adage: location, location, location! Buy or build facilities where the demographics are favorable. Offer the features today’s young consumers want: convenience, technology, and value. If your local market has a significant segment of millennials, be sure to lead with technology and sustainability in your marketing.

- Millennials are more likely to live in apartments than older generations.

- They are more likely to live in urban areas.

- Apartments are getting smaller, especially in urban areas.

- Self-storage costs up to 30 percent less than apartments by square feet.

Millennials store their kayaks and snowboarding equipment, which they use often. This means they go to their units more often than baby boomers, who don’t tend to visit their stored memories.

Using storage units more like an extra closet, millennials visit more frequently to swap out clothing, furniture, holiday decorations, and other “season of life” items, such as baby furniture, car seats, and toys. All of this generates more traffic at self-storage facilities from millennials than older generations.

Younger renters tend to rent less costly, smaller units (10-by-10 or smaller), and they expect to be there for shorter periods of time. While these tendencies may generate less rental revenue for the facility, younger renters generate more ancillary revenue through purchases of items they need for storage, like boxes, tape, and packing supplies. They are also more likely to rent trucks than older renters.

They also want more flexibility in contract terms, pricing, and means of payment, including a wide variety of payment options, from autopay via debit or credit card, to Apple Pay and Google Pay. They want to be able to get in and out of contracts easily, and they want to be able to lock in pricing.

Millennials also place greater value on temperature and humidity control, as well as in-unit fire sprinklers and security features.

Finally, especially in dense urban areas, younger renters are more likely to walk, bike, or take public transit to their storage units. Not many boomers do that!

They want to be able to do every step of the rental process from their beds, on their phones, at any time. That means comparing facilities, reading reviews, selecting a facility, selecting their space, signing the lease, obtaining access to their space, buying merchandise, and renting a truck.

Even if they don’t do all those steps every time, they want to be able to do it all 24/7. Excellent digital presence and functionality, including online rentals, are critical for younger renters.

In terms of cities, regardless of generation, the biggest winners were Seattle, Wash.; Nashville, Tenn.; and San Antonio, Texas. Generally, the biggest losers were New York, N.Y.; Los Angeles, Calif.; and Portland, Ore. Of all U.S. cities, more people moved out of New York City than any other.

According to the data, cities people are moving to and from vary greatly by generation. For instance, Seattle returned to the top spot in 2022 for millennials, after falling to No. 115 in 2021, but not for Gen Z. Seattle wasn’t even in their top 10 cities.

Gen Z is the only generation that seems to be flocking to more well-known big cities, especially Washington, D.C. This leaves people wondering if DC is the new NYC for Gen Z. Also in Gen Z’s top 10: Chicago, Ill.; Boston, Mass.; New York, N.Y.; Philadelphia, Pa.; Los Angeles, Calif.; Tucson, Ariz.; Eugene, Ore.; and Columbia, S.C.

Tracking with older generations, millennials left major cities such as New York, Los Angeles, Philadelphia, and Las Vegas. In fact, while New York was the top spot for millennials to move to in 2012, it was the top spot for millennials to move out of a mere 10 years later in 2022, for the second year in a row.

Overall, in 2022 millennials tended to move to tech-hub cities with thriving arts communities. Seattle in the top spot, followed by Austin, Texas; Nashville, Tenn.; Charlotte, N.C.; and Denver, Colo.

Summarizing migration data, younger renters are moving into Seattle, Austin, Nashville, Charlotte, and Denver (millennials), as well as D.C., Chicago, Boston, New York, Philadelphia, Los Angeles, Tucson, Eugene, and Columbia (Gen Z). That covers a lot of territory!

Facilities in these locations will find it especially important to remember that younger renters are more likely to be:

- Female

- Racially diverse, particularly Hispanic

- Living in rental properties

- Living in urban areas

These younger renters tend to:

- Use self-storage as an extension of their homes

- Rent smaller units that cost less

- Buy more merchandise and rent trucks more frequently

- Pay a premium for tech and sustainability

- Visit their units more frequently

Both millennials and Gen Z expect convenience, including short driving distances. They are willing to pay for technology and sustainability, and they are more demanding about the features and amenities they want.

In general, everything they want is likely to be in greater demand in the future, so making your facility attractive to younger renters positions you well for generations of the future. This way you can meet the market where it is going, as future renters will all increasingly rely on high-tech solutions for every aspect of daily life.

he self-storage industry experienced a surge in demand during the pandemic, but that robust growth has ended. Operators are now grappling with fewer move-ins, declining rental rents, and rising vacancies. The intensified competition triggered a pricing battle among the major players, with each rate cut frequently causing a full-fledged price war across numerous markets.

While the temptation to slash prices to capture customers is understandable, price competition is usually a “negative sum” game that erodes long-term profitability. Cutting prices is easy to implement, but assessing their long-term effects is challenging. Furthermore, reversing the negative revenue consequences of substantial price cuts can be slow and arduous.

Being market-aware and knowing when and where to respond to competitive price changes is crucial. This involves understanding how competitive pricing influences customer demand for your products and responding selectively. Sometimes, the most prudent course of action is ignoring competitors’ price cuts. However, in other cases, offering lower prices or matching competitors’ pricing is necessary.

This article explores proven strategies self-storage operators can adopt to navigate the competitive landscape without resorting to destructive price wars. Operators can achieve sustained growth and success by focusing on non-price actions, implementing pricing segments with differentiated offerings, and optimally responding to competitive rate modifications.

- Occupancy Concerns – Occupancy drops when move-outs outpace move-ins. Anxious about their stock prices, publicly traded REITs reduce street rents and increase marketing expenditures to safeguard occupancy levels.

- Revenue Juggling – To mitigate the revenue loss, REITs often implement aggressive rate hikes for their existing tenants shortly after move-ins. Although this approach may generate customer backlash and affect brand perception, REITs estimate positive net revenue as the number of tenants vacating due to rate hikes may not be substantially higher than the number of tenants leaving naturally.

- Hedging – Large operators do not uniformly reduce rates across their entire portfolio. Instead, they keep higher rates in select locations and products while implementing more substantial rate reductions in others. This strategic approach allows them to hedge against market fluctuations and protect overall rates and revenue.

- Slow Response From Smaller Operators – Many independent operators lack sophisticated revenue management systems and cannot promptly and optimally react to rate changes. This delay grants REITs a competitive advantage and allows them to gain a foothold in the market.

Actions unrelated to pricing include honing digital and other marketing tactics, enhancing brand presence, raising value awareness of your offerings, improving customer service, and modernizing technology-based capabilities such as websites and AI-based revenue management. While these endeavors typically build long-term capabilities, you could potentially achieve improvements in these domains in the short term. These initiatives represent “positive sum” forms of competition and should always be on the radar.

Continuously Assess The Impact Of Competitive Price Changes

The alternative strategy is to reduce prices. While cutting prices can be straightforward, the challenge lies in assessing the consequences of price reductions. It is vital to analyze whether such rate moves boost occupancy and whether the increased move-ins compensate for the reduced yield. Furthermore, the strategy requires monitoring the impact of lower prices, especially if competitors respond with further rate cuts.

Neglecting competitors’ pricing actions can be risky, but copycatting is as risky since it often entails delegating the price-setting responsibility to competitors. Instead, we recommend a surgical approach to price adjustments, carefully evaluating the impact of competitive price changes on your demand.

We utilized AI-based revenue management models, analyzed extensive market data involving thousands of stores across diverse self-storage markets, and found varying impacts of competitive price changes on customer demand. In half of the products, competitive price changes have little or no effect on demand, and 30 percent of the products have high degrees of impact.

AI-based revenue management provides these kinds of granular analyses to gain insights into each competitor at both store and individual unit type levels, enabling surgical responses to competitive price cuts, ensuring command over your pricing tactics, and optimizing your financial performance.

Harness The Power Of Price Segmentation

In the event of competitive rate reductions, we strongly encourage avoiding the across-the-board rent cuts. Instead, we recommend a selective pricing response based on the following pricing segmentation strategies, which can be employed individually or in combination.

- Store Types – Emulate hotel chains by creating distinct name brands for your self-storage facilities based on quality, demographics, and other store attributes (E.g., Class A and Class B). You can, for example, aggressively compete for Class-B facilities while safeguarding your rates for your Class-A facilities.

- Unit Types – Differentiate your unit types based on size and features such as climate control, drive-up access, floor levels, and convenience. We employ sophisticated value-based pricing by defining sufficiently differentiated unit types and offering highly competitive prices for lower-tiered, harder-to-sell units while maintaining higher rates for premium units.

- Promotions – Leverage extensive upfront offers or discounts while protecting your street rates. Customers tend to overestimate the value of upfront discounts since they stay longer than they initially anticipated. This approach incorporates the length-of-stay distribution of the customers in each store, unit type, and customer type.

- Sales Channels – Implement distinct pricing strategies through sales channels like in-person, online, and third-party partners. We recommend being aggressive with your pricing online or with third-party partners while maintaining higher rates for in-store sales. You can optimize street rates and use them as strike-through prices to anchor online sales and utilize them for in-store sales or your existing customer increases.

- LOS Pricing – Offer aggressive pricing for customers who commit to a minimum length of stay. While it is not widely utilized, some operators have employed this approach in certain countries and markets.

While all-out price wars may attract customers in the short term, they are “negative sum” games that destroy profitability and often prove unsustainable in the long term. The relentless focus on price can lead to a race to the bottom. This downward spiral can damage brand reputation and hinder long-term growth.

To avoid the pitfalls of price wars, we recommend that operators adopt a more strategic approach to pricing and first consider “positive sum” forms of competition in marketing, branding, operations, customer service, and technology opportunities.

However, it is sometimes impossible to ignore the competitive rate cuts and necessary to compete on price. In such situations, it is best to avoid blanket rent reductions across their entire portfolio. Instead, we recommend offering complex pricing options by sales channels such as walk-ins, online, and third-party partners. Operators can also employ localized pricing actions based on store, unit type, and customer type to strategically lower prices and offer enticing introductory promotions for specific segments or products facing competitive pressure. Furthermore, it is critical to continue optimizing existing tenant rent increases. Remember, while occupancy matters, the ultimate goal is to maximize long-term revenue and profits.

veryone in the industry is aware that divorce is one of the many demand drivers for self-storage. Divorce generates demand while couples resituate themselves into new residences and sort through their belongings. Temporary (and oftentimes smaller) living arrangements may require individuals to place their excess belongings into storage for a few months or longer. Although divorce is typically associated with loss, sometimes one man’s misfortune is another man’s (or company’s) gain. As a matter of fact, it was divorce that altered the course of business for Emeryville, Calif.-based Devon Self Storage Holdings LLC (formerly known as Devon Capital Management LLC).

Devon, which Kenneth E. Nitzberg, chairman and CEO, founded in 1988, was originally focused on office, retail, and multifamily commercial real estate. It’s first foray into self-storage, however, was “by accident.”

As Nitzberg recalls, the year was 1993, and one of Devon’s real estate acquisition officers was in the throes of a divorce. He was “kicked out” of his former home and needed to store his possessions, but he couldn’t find a single storage unit to rent in the then small community of The Woodlands, Texas.

veryone in the industry is aware that divorce is one of the many demand drivers for self-storage. Divorce generates demand while couples resituate themselves into new residences and sort through their belongings. Temporary (and oftentimes smaller) living arrangements may require individuals to place their excess belongings into storage for a few months or longer. Although divorce is typically associated with loss, sometimes one man’s misfortune is another man’s (or company’s) gain. As a matter of fact, it was divorce that altered the course of business for Emeryville, Calif.-based Devon Self Storage Holdings LLC (formerly known as Devon Capital Management LLC).

Devon, which Kenneth E. Nitzberg, chairman and CEO, founded in 1988, was originally focused on office, retail, and multifamily commercial real estate. It’s first foray into self-storage, however, was “by accident.”

As Nitzberg recalls, the year was 1993, and one of Devon’s real estate acquisition officers was in the throes of a divorce. He was “kicked out” of his former home and needed to store his possessions, but he couldn’t find a single storage unit to rent in the then small community of The Woodlands, Texas.

An unfinished strip shopping center on a five-acre lot was on the market for $600,000 through the Resolution Trust Corporation, a quasi-governmental agency formed to relieve the mutual savings banks of their failed real estate loan. The center had 50,000 square feet of space and only four month-to-month retail tenants, including a nail salon, a hair salon, a light bulb store, and a cookie shop, but instead of going the retail route, the divorcé was instrumental in pushing Devon towards transforming it into a self-storage facility. Devon decided to take a risk. They purchased the building for $600,000, borrowed $1 million from Wells Fargo Bank to fund the conversion of the building into self-storage, and then flipped it 40 months later to what is today CubeSmart (formerly U-Store-It Trust) for $4 million.

“We did nothing but storage after that,” says Nitzberg. “We thought we had found the ‘holy grail’ of self-storage by discovering that we could purchase a vacant building at a very favorable price from a distressed owner as the building had failed in its financial objectives and then convert it into a state-of-the-art self-storage asset. Essentially, we were buying storage assets on a wholesale basis versus a retail cost basis.”

Then, in 1998, Goldman Sachs stepped up and acquired a 90 percent interest in Devon Self Storage. At the time of the sale, the company was operating 20 properties for three institutional investors and several smaller private investors. Through Goldman Sachs’ Whitehall Fund XI, $83 million was used to acquire 16 facilities over a three-year period, six of which were in Holland, France, and Germany; the other 10 assets were in the U.S.

Devon’s presence in those countries prompted Nitzberg to assist with the development of the Federation of European Self Storage Associations (FEDESSA), which presently represents 2,000 facilities or more than 70 percent of Europe’s self-storage sites. Various Devon employees were very instrumental in the formation of the FEDESSA, particularly in its formative years. He also served as chair of the Self Storage Association (SSA) in 2006 and was inducted into its Hall of Fame in 2015. Moreover, in 2023 Nitzberg was the third person to receive the Michael T. Scanlon award for his contributions to the SSA.

Although conversions had been Devon’s “main business,” Nitzberg mentions that the company did execute “some scrape and rebuilds,” as well as the acquisition of a number of existing self-storage facilities. Devon also managed more than $1 billion of real estate assets, including a portfolio with 20 self-storage properties from 2009 to 2011, on behalf of several CMBS special servicers. (A CMBS special servicer assumes servicing responsibility for defaulted CMBS loan or loans that are at risk of default.) Devon Self Storage ended up buying several of those properties and subsequently sold them a few years later, after filling them and bringing the respective NOIs to market levels, thus generating significant profits.

The Tax Cuts and Jobs Act’s (TCJA) creation of Qualified Opportunity Zones in 2017 further fueled Devon Self Storage’s preference for conversions. “The tax benefits are substantial,” Nitzberg says about investing in real estate within low-income communities that have been designated as distressed based on the 2010 Census data. Many of those communities have undergone significant economic improvements since the census was finalized. Investments in Opportunity Zones also spur economic growth and job creation. Plus, there’s an abundance of possibilities with 8,764 Opportunity Zones in the United States.

Throughout its 31-year history, Devon has owned, managed, or developed more than 350 self-storage facilities in 27 states and three European countries. What’s more, Devon Self Storage has been present on Messenger’s annual Top Operators list numerous times.

Inland Private Capital Corporation President and CEO Keith Lampi was hopeful that Devon might have interest in partnering on Inland’s strategic entry into the sector, but “I told him no,” says Nitzberg. “We had just bought a 22-property portfolio from CubeSmart and didn’t have the bandwidth. Inland then did about 84 deals with others.”

According to Matthew Tice, senior vice president at Inland Real Estate Acquisitions, LLC and co-CEO and president of Devon, the two firms eventually reconnected through Inland’s acquisition of the very same 22-propertry portfolio that led Nitzberg to turn Inland down in the first place.

In 2020, the two companies formed a development strategic relationship aimed singularly at acquiring conversion candidates in Opportunity Zones. Inland raised $100 million through a private fund and charged Devon with sourcing, acquiring, and converting those assets into self-storage assets. When that fund’s capital was fully raised, Inland exercised its “green shoe” to increase the offering to $150 million, which was completed September 2021. Inland still had an appetite for additional Opportunity Zone assets, so a new fund was formed, and it raised an additional $100 million around the same storage re-development strategy.

With the $250 million of new capital, Inland, through its relationship with Devon, acquired 15 assets. Eight have been converted and opened for leasing; seven are still under construction, but all of them should be completed in 2024 and open for leasing. These two programs provided a significant boost in Inland’s growth trajectory in the self-storage sector.

Since entering the self-storage sector in 2016, Inland has amassed a $1.7 billion self-storage portfolio of both stabilized assets and development projects across 30 states. As of February, they had a total of 98 operating facilities and 13 under construction with Devon and 87 assets with other property management companies.

“For over 30 years Devon has been doing what we do best: acquiring, redeveloping, and operating high-quality self-storage properties,” Nitzberg said in the press release that heralded the news. “I am thrilled to continue that work with Tony [Chereso, Inland’s Chief Executive Officer], Matt [Tice], Keith [Lampi], and the entire Inland team as well as Devon’s more than 270 employees dedicated to delivering best-in-class self-storage properties and services.”

According to Tice, the acquisition allows Inland to leverage Devon’s existing senior management team, which has been together for more than two decades, while at the same time providing additional capital and infrastructure necessary to further drive the going-forward platform’s innovation and expansion plans including growth of Devon’s third-party management and development platform.

“It was the right time to form an integrated partnership,” says Tice. “Inland has internal entities and its own staff to augment Devon.”

“Devon has been an integral strategic partner as Inland has expanded our presence in the self-storage sector,” Lampi, said in the press release. “As the sector continues to institutionalize, creating operational efficiencies for the benefit of our investors through scale has never been more important. I am looking forward to the synergies created by this transaction.”

Those synergies will enable Devon to eventually take over the management of Inland’s other 87 self-storage assets. The facilities currently being managed by other companies will “all transfer to Devon by the end of 2025,” says Tice.