elf-storage adaptive reuse has gained significant popularity as an effective way for developers to add new inventory. This approach rose alongside the sector’s rapid growth, as self-storage expanded beyond its traditional use encapsulated by the four Ds. Homes have been trending smaller, and storage units have gradually become an extension of the home, supporting items that no longer fit into living spaces.

While demand has continued to rise, limited land availability and restrictive zoning laws are among the key hurdles preventing ground-up construction from keeping pace. As a result, developers have increasingly turned to adaptive reuse as a viable alternative, particularly in markets where vacant industrial buildings, retail stores, and other property types offer a clear path to adding new storage space through conversions.

See Top Building Types Converted into Self-Storage chart.

See How Self-Storage Conversion Deliveries Have Evolved by Decade chart.

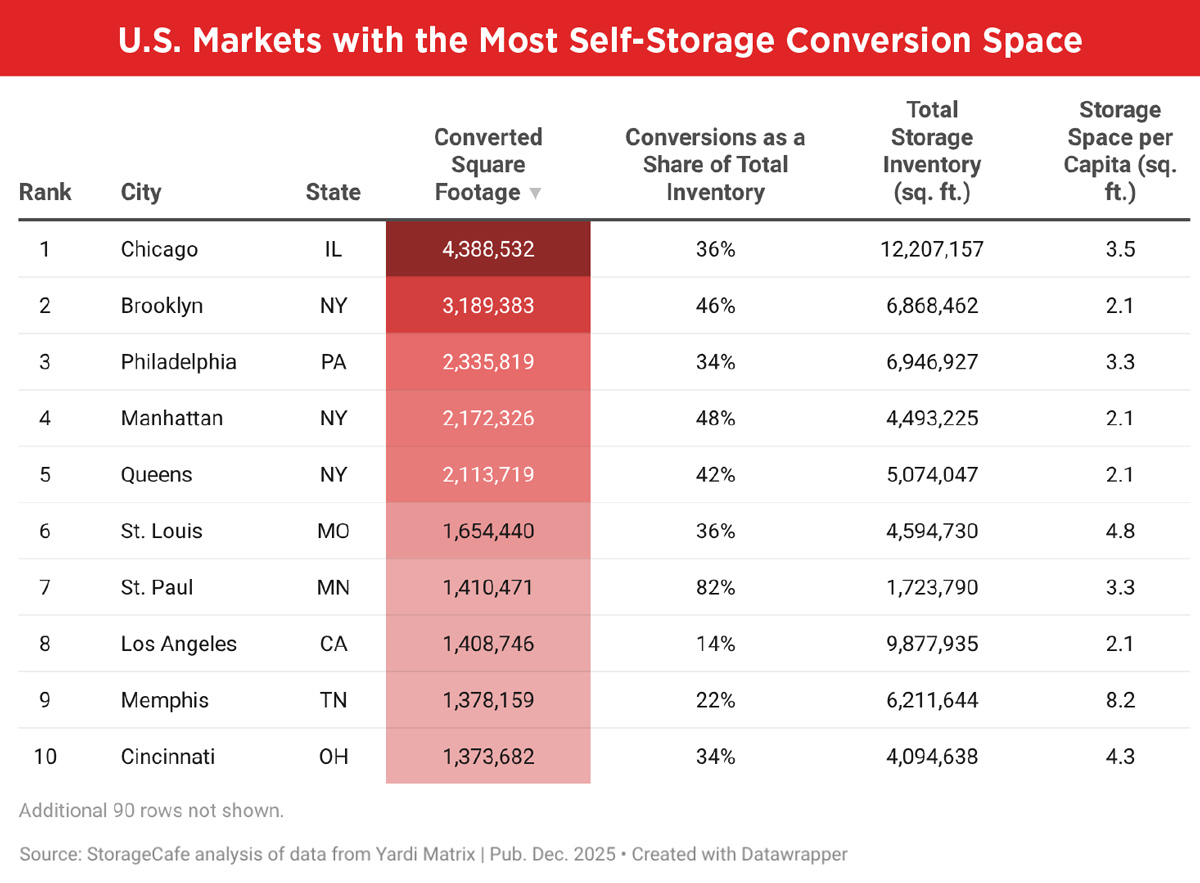

See Under-Construction Conversions and Key Metrics Across U.S. Cities and U.S. Markets with the Most Self-Storage Conversion Space tables.

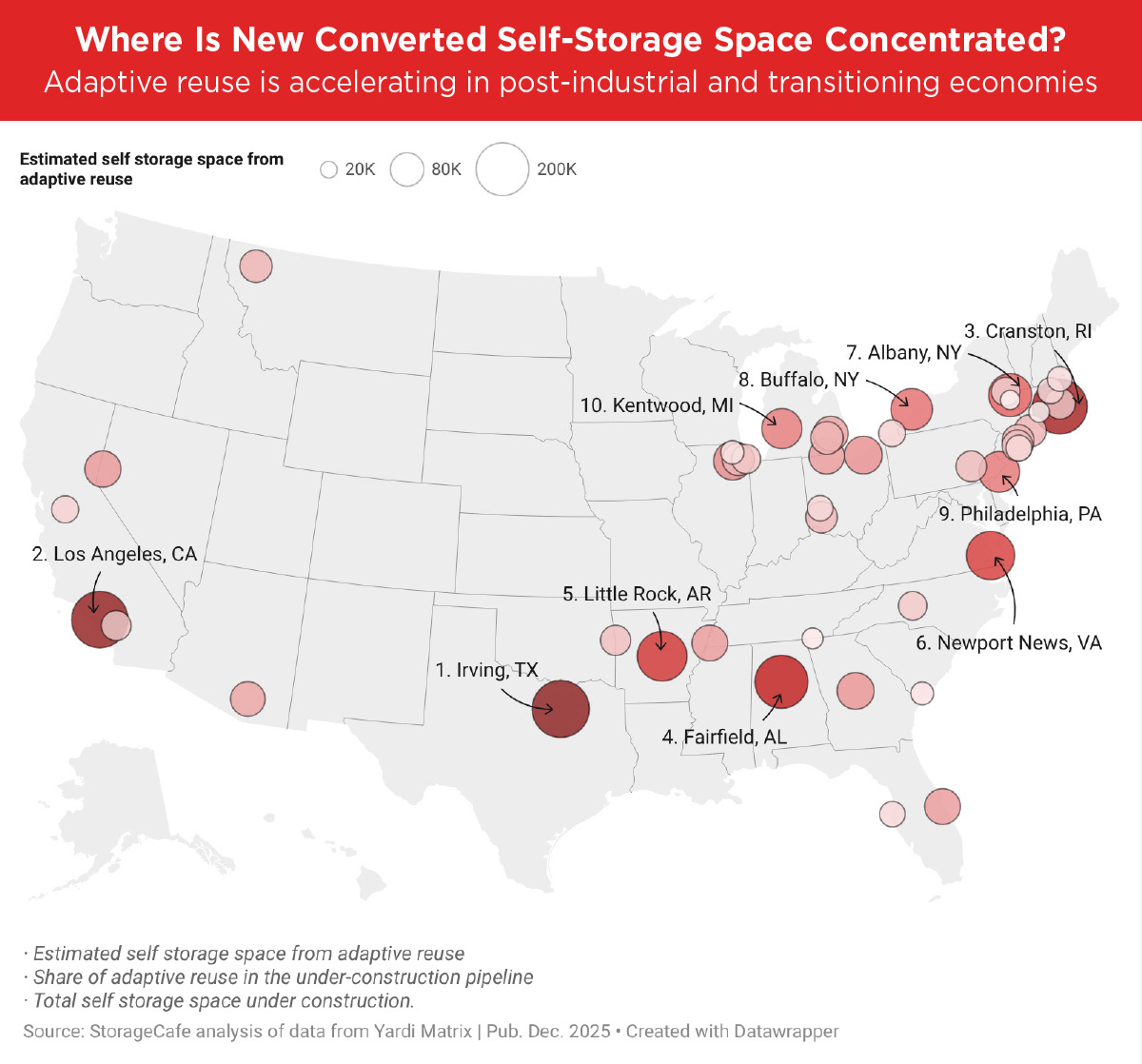

Population growth continues to support demand, with Irving’s population rising nearly 7 percent over the past five years. In this environment, conversions offer a faster and more flexible way to add supply. Nearly all the city’s conversion pipeline comes from retail properties, which account for about 95 percent of projects, largely driven by local store closures that created adaptive reuse opportunities.

Los Angeles, Calif., is another leading market for conversion projects under construction. With only 2.1 square feet of self-storage per capita, the city remains severely undersupplied, making the addition of 226,000 square feet of storage space a meaningful boost. This volume represents almost 60 percent of all storage space currently under construction in Los Angeles.

Overall, the city has delivered approximately 1.4 million square feet of self-storage through conversions, most of which originated from office buildings, followed by industrial properties. The prevalence of adaptive reuse has also helped create a more renter-friendly environment, with average street rates in LA at converted facilities reaching $221 per month—about 7 percent lower than rates at purpose-built properties.

Fairfield, Ala., is another strong performer, with more than 200,000 square feet of conversion space expected to come online, accounting for the city’s entire under-construction inventory. Fairfield currently offers just 2.2 square feet of self-storage per capita, making conversions an efficient solution for expanding its limited supply. The city already has close to 114,000 square feet of conversion inventory, all sourced from former retail properties following closures such as Walgreens, Francesca’s, and others.

Conversions offer a practical solution for adding inventory in these markets, where land constraints and zoning regulations often complicate ground-up development. Cranston, R.I., stands out as the only East Coast city with more than 200,000 square feet of self-storage under construction through adaptive reuse—a figure that also represents its entire development pipeline. This new supply will help offset a limited existing inventory of just 1.2 square feet per capita. Converted facilities in Cranston also offer lower costs, with average monthly rents of $119, roughly 26 percent below those of ground-up properties.

Newport News, Va., is set to add close to 165,000 square feet of storage space, accounting for more than two-thirds of the city’s under-construction inventory. With more than 6 square feet per capita, Newport News has the highest inventory relative to population among high-performing East Coast cities. Demand remains supported by nearby military installations, which continue to drive development activity.

In New York state, Albany and Buffalo are also contending with inventories below 4 square feet per capita, sustaining ongoing development. Albany is adding nearly 129,000 square feet of storage through conversions, while Buffalo is close behind with approximately 119,000 square feet. In both cities, industrial properties dominate conversion projects. All of Albany’s existing adaptive reuse inventory is located within opportunity zones, underscoring a focus on urban revitalization, while about 60 percent of Buffalo’s conversions are similarly situated.

See Where Is New Converted Self-Storage Space Concentrated map.

Oak Park and Westland, neighboring suburbs in the Detroit metro area, are also seeing notable conversion activity. Oak Park has more than 81,000 square feet of self-storage under construction, all originating from office buildings. Westland is adding close to 70,000 square feet of converted space, sourced entirely from former retail properties following multiple closures, including the Westland Center Mall.

Adaptive reuse has established itself as a viable way to add new inventory, especially in markets where demand is high and traditional development faces numerous hurdles. Across the Sun Belt, East Coast, and Midwest, conversions are helping cities respond to sustained demand by unlocking underutilized retail, office, and industrial buildings and bringing new inventory online more efficiently, remaining a pivotal inventory growth pathway in the sector.