ne thing is certain: We’re surrounded by uncertainty. Input from over a dozen self-storage owner-operators and five REITs confirms this. Nonetheless, they all still need to run their businesses, so understanding how today’s down economy impacts self-storage is very important.

With an election pending and the economy in a slump, how is our inflation- and recession-resistant asset class faring? It depends on who you ask. Inputs from operators of all sizes and all parts of the country range from good or steady to down and way down.

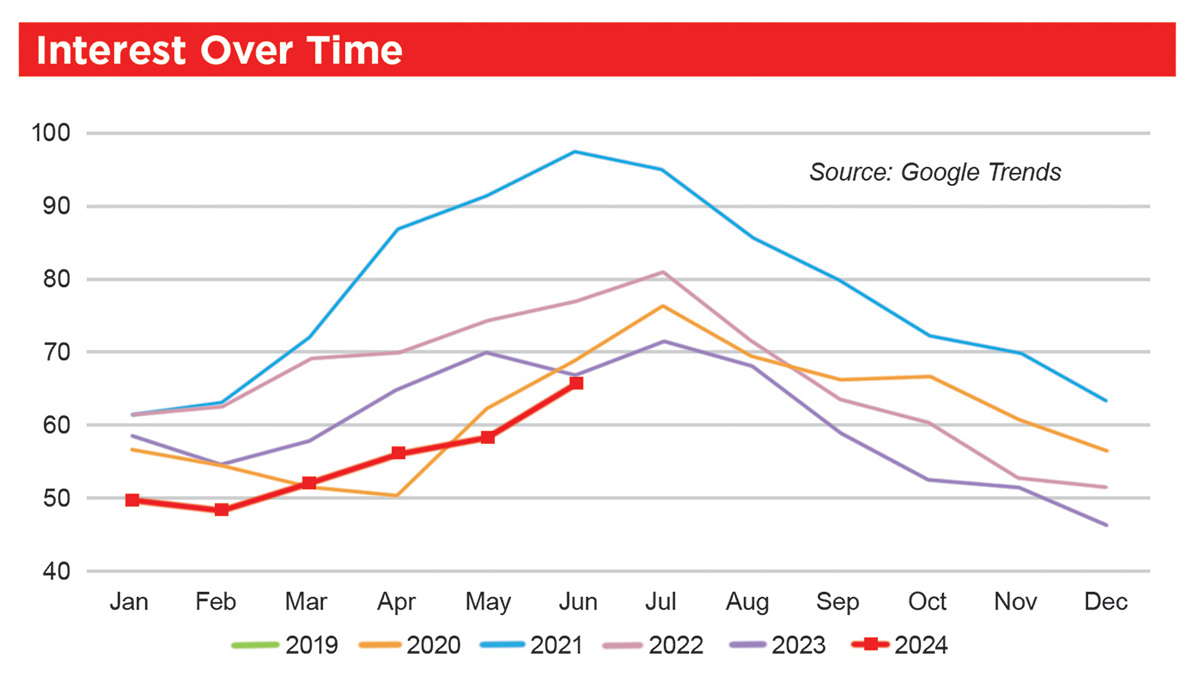

See Interest Over Time Chart

To clarify, demand for storage is not down everywhere. We all know self-storage is a local market. Most renters are within a 3-, 5-, 10-mile radius of their facility and have a reasonable drive time (20 minutes or less). So national trends should be taken with a grain of salt, because some local markets are thriving in today’s economy. However, others are not; overall, demand for storage is down, especially compared to the COVID highs of recent years.

See U.S. Home Price Chart

“Moving is one of the biggest reasons people rent self-storage. Demand is absolutely down,” said Eva Chavez, founder of Beacon Ave Marketing, a digital marketing agency focusing on the self-storage market. Chavez works with facilities all over the U.S. “Millennials are stuck due to the real estate market. Without change, there’s no extra need for storage.”

Moving is not the only reason to rent self-storage. Life events such as getting married or divorced, having children or children moving back home, adding aging parents to the home, and death of a loved one also create demand for self-storage. “But even that is lower than before,” said Chavez, who has tracked leasing seasons for years. This year’s leasing season started later and did not peak as high as previous years, according to Chavez, who added that even stores where street rates have dropped dramatically did not receive a significant amount of move-ins as a result.

Pam Domingue, owner of eight Storage Solution facilities, agrees that demand is down, with occupancy down a few percentage points and delinquency up a few percentage points over 30 days. She notes that more delinquent units are going to auction than in the past, when people were more likely to come in and pay. “People seem to be more willing to walk away from their stuff,” said Domingue.

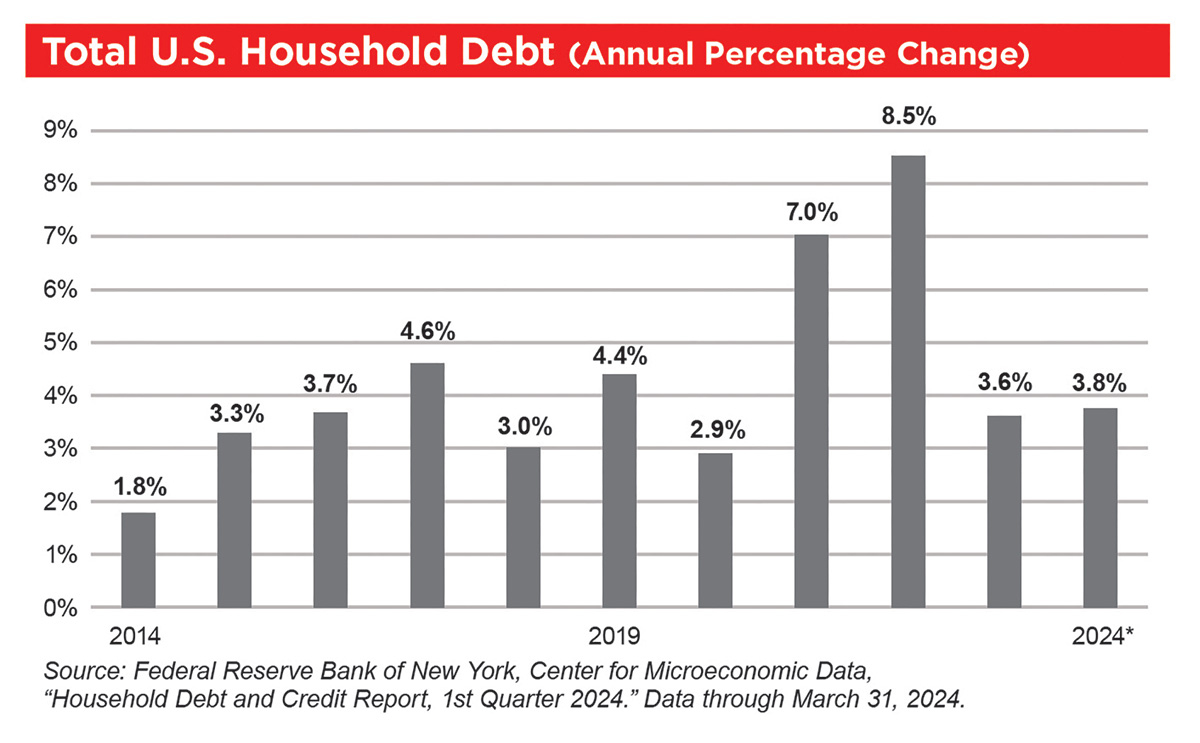

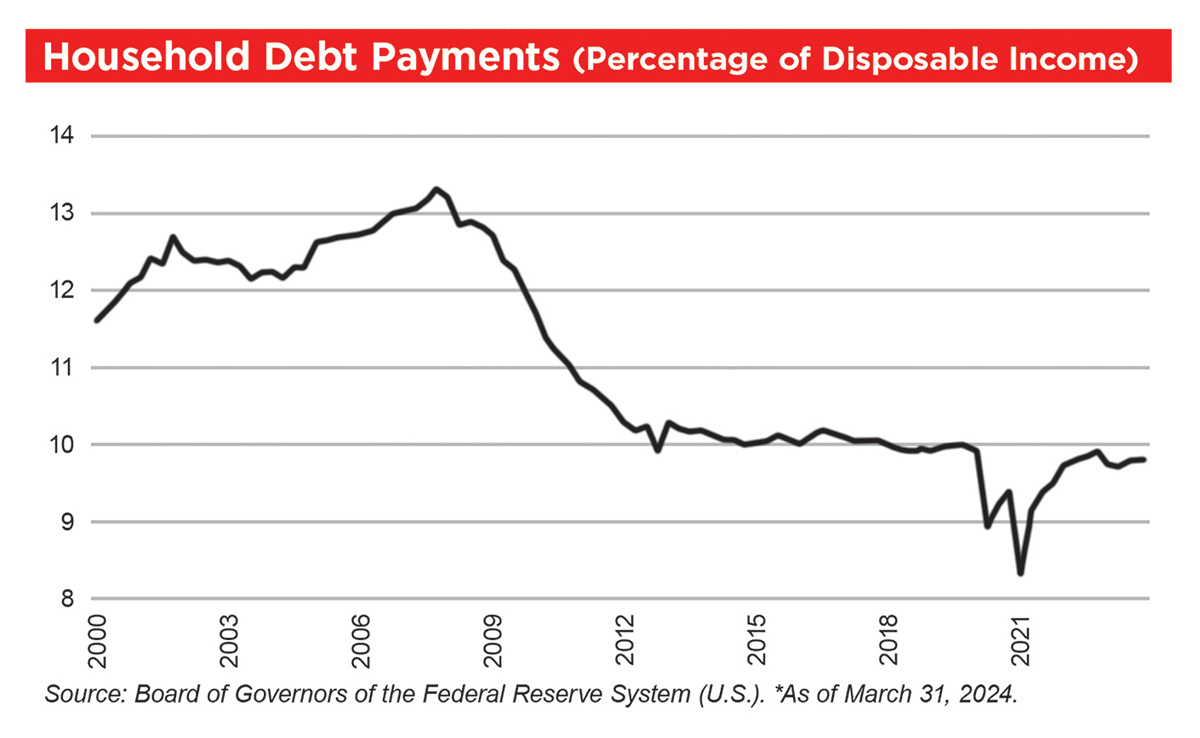

See Total U.S. Household Debt Chart

Adding perspective, while consumer debt is up since 2021, it is still less than 10 percent of disposable personal income, which is significantly lower than the 13 percent level from 2007 and 2008. Experts don’t seem to be worried about the 3 percentage points that separate today’s rate from that of the Great Recession.

See Household Debt Payments Chart

Other large storage operators and vendors providing services in accounts receivable (AR) and collections seem to agree. They report no significant increase in delinquency this year. Fredrik Velander is the co-founder of AI Lean, which offers a streamlined end-to-end lien to auction process. He has a view into AR across the country and indicates that delinquency did not change significantly since the beginning of the year. Likewise, occupancy remained consistent from Q1 to Q2 of 2024.

Domingue adds an important point to the demand discussion: “Part of it is that prices are up, and we are pricing people out. Price is driving us now, and we did it over the last three years.” Some people who used to be able to afford self-storage are not able to in today’s market, where more people describe themselves as living paycheck to paycheck.

Diane Gibson, president of Cox’s Armored Mini Storage Management, shared her thoughts on how we have historically viewed the self-storage market and how that compares to today. “In bad times, self-storage is a necessity. We’re not seeing that yet,” she says. “We’re seeing it is a luxury, so some people are moving out.” Gibson and her team carefully track why renters move out, and this is what the data is telling them.

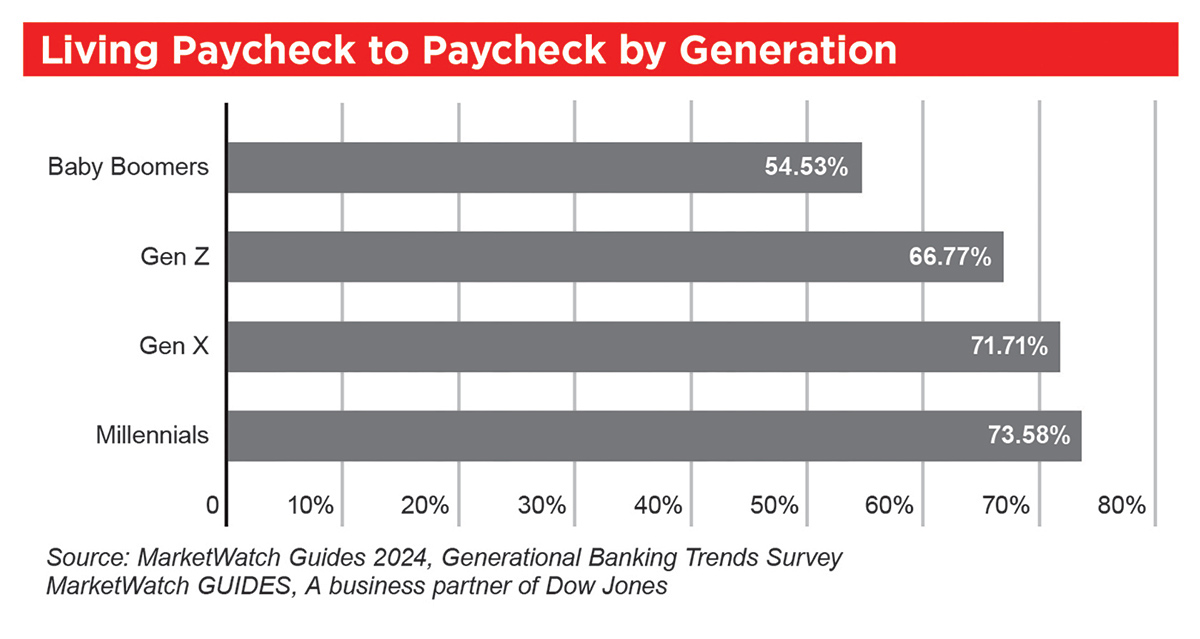

What about the bigger picture? According to a recent survey by MarketWatch Guides, 66.2 percent of Americans feel like they are living paycheck to paycheck. The Living Paycheck to Paycheck chart shows this sentiment by generation.

See Living Paycheck to Paycheck Chart

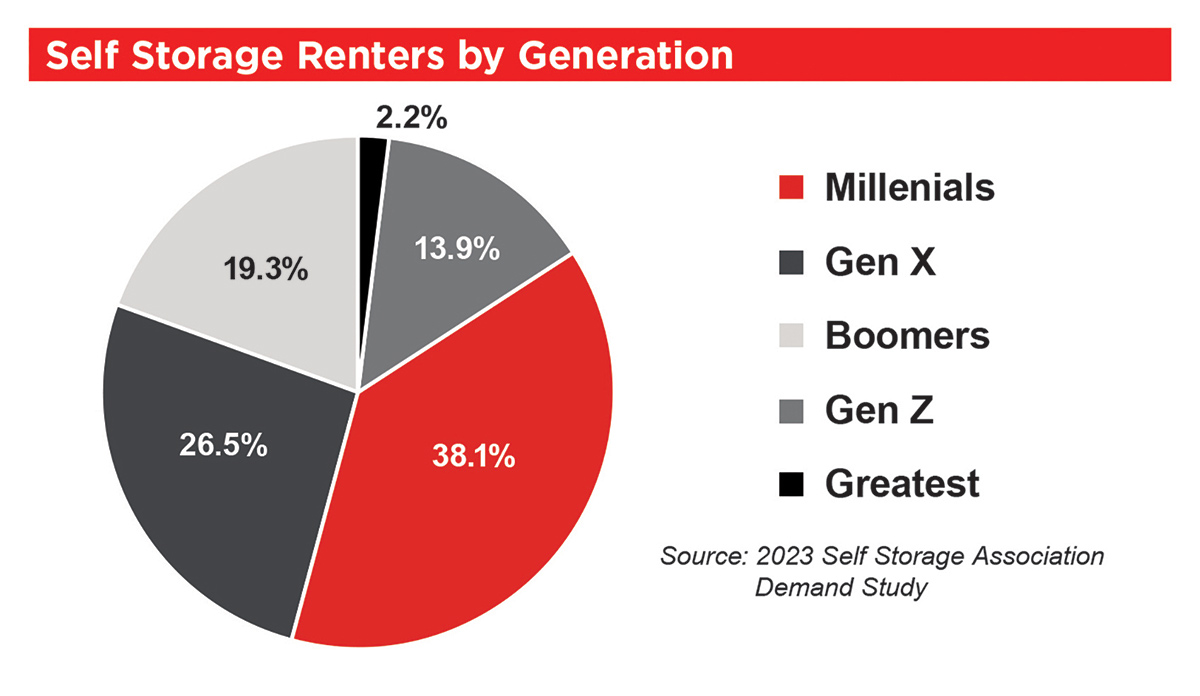

See Renters by Generation Chart

Gen X also feels financially insecure, with a whopping 71.71 percent saying they live paycheck to paycheck. They are the second-largest generation of self-storage renters at 26.5 percent.

As for Gen Z, 66.77 percent describe themselves as living paycheck to paycheck. They represent 13.9 percent of renters.

If almost 79 percent of self-storage renters fall into these three generations, clearly many of our customers feel like they are living paycheck to paycheck. It’s not a stretch to conclude that they feel priced out of self-storage, especially since in-place rent skyrocketed so dramatically in recent years.

“Major, readily apparent growth trend” certainly describes self-storage development in the past 10 years. “… 462 million square feet of new self-storage space was delivered between 2013 and 2022, representing 25 percent of the total inventory,” according to CommercialSearch, Aug. 16, 2023.

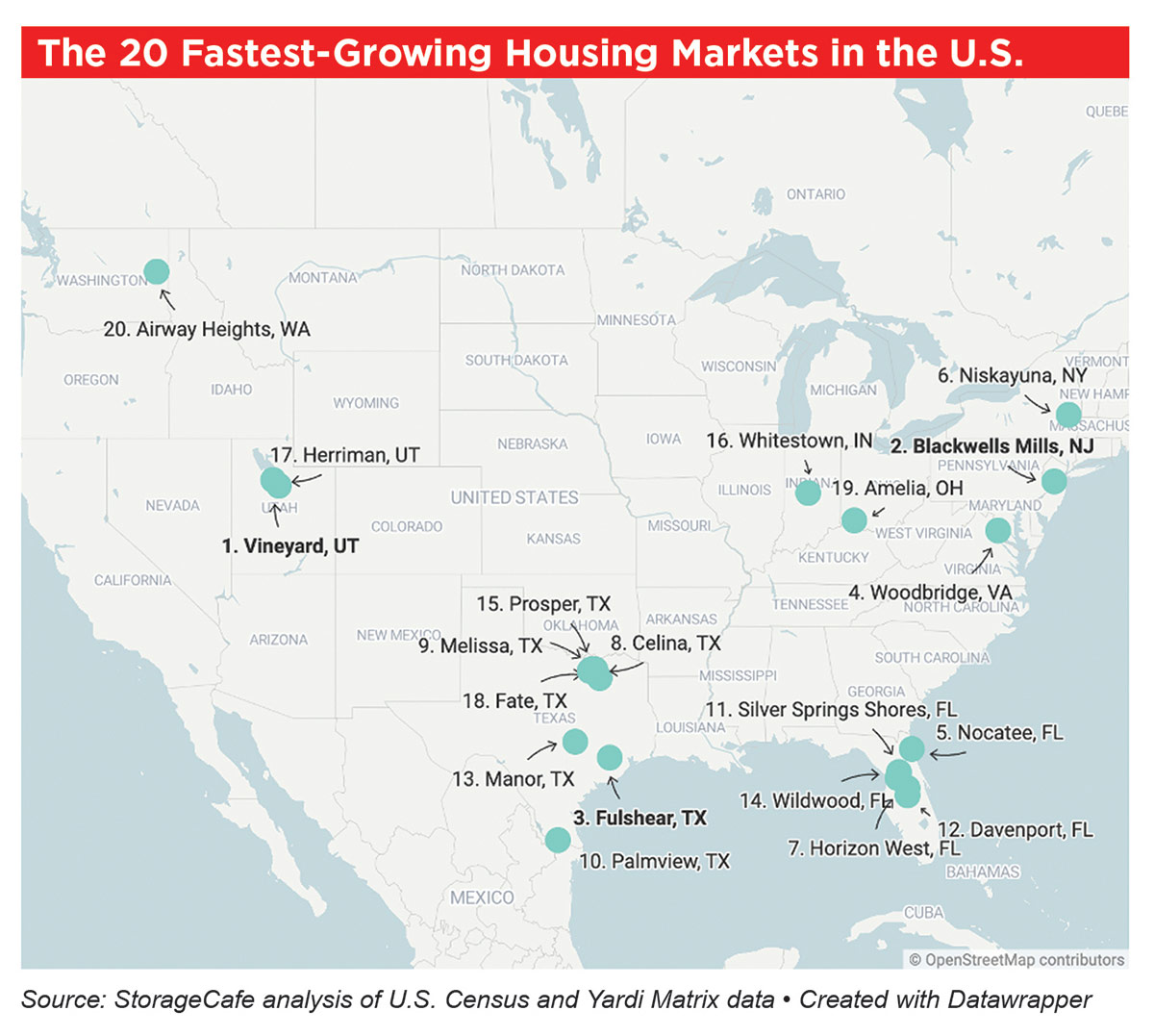

Were investors tending to move in the same direction at the same time? A great deal of new self-storage supply was added to the 20 fastest-growing U.S. housing markets over the past 10 years.

See The 20 Fastest-Growing Housing Markets in the U.S. Map

See Top 10 Cities for Self-Storage Industry Expansion Chart

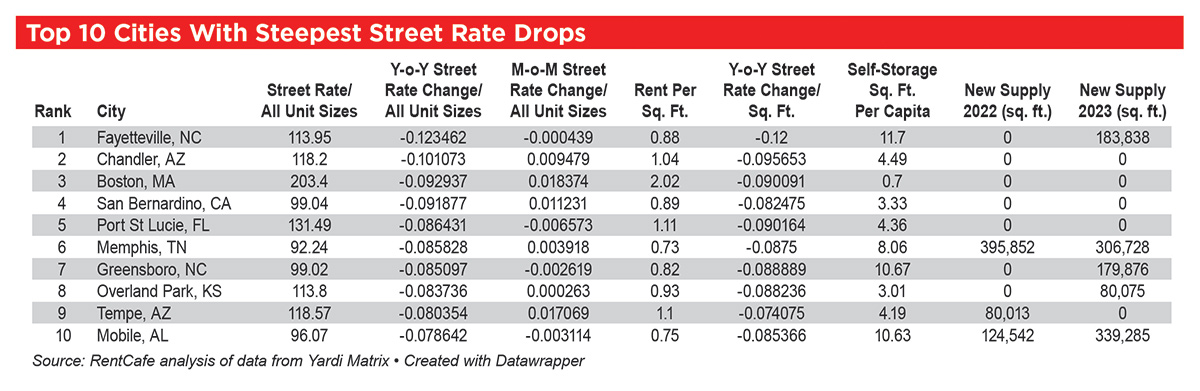

See Top 10 Cities With Steepest Street Rate Drops Table

- Yonkers, in the New York Metro Metropolitan Statistical Area (MSA)

- Three Arizona cities in the Phoenix MSA

- Three Florida cities, including Orlando

So yes, rates are falling in these markets, and overbuilding is one of the causes. It seems that investors have tended to move in the same direction at the same time, and falling rates are following them.

Most experts agree that new supply will be absorbed within a few years. Operators tend to expect it to take about 36 months for rates to recover after new supply is delivered to their local 3-, 5-, 10-mile market. Equilibrium will return, but for operators in those 36 months right now, in local markets where supply is up and overall demand is down, it hurts. It hurts even more if they need to convert short-term debt to permanent financing with higher interest rates.

Radius+ reports street rates by tracking data on REIT asking rates in the top 25 U.S. markets.

According to Radius+’s June 2024 report, the price per square foot for a 10-by-10 climate-controlled unit was $1.35. That is a 14.4 percent drop since June 2023. April and May saw similar year-over-year drops, which are an improvement over the 16 percent, 17 percent, and 18 percent drops in January, February, and March of 2024.

But what’s really interesting is comparing the $1.35 price per square foot in June 2024 to pre-COVID years. Radius+’s June 2023 report indicates that in 2019, the price per square foot was $1.37, which is two cents higher than 2024. Can you think of anything else in your world or operations that costs less now than it did before COVID? I can’t.

- Self-storage is hyper local.

- A facility’s performance depends on how well you operate it.

Hyper local to its core, each self-storage facility has a trade area of 3, 5, or 10 miles, or 20-minute drive times. The better your local market, the better your business.

Operational excellence is the cream that rises to the top. During the COVID years, every self-storage business benefitted from the industry’s increased occupancy and rental rates. That era is over. Self-storage performance today is also highly dependent on operations: Strong operators have better performing businesses. Operational excellence is critical, including marketing and customer service that turns leads into renters.

Overall demand for self-storage is down, but that doesn’t mean storage is performing poorly. On the contrary, many operators report that even though street rates are lower, and the 2024 rental season has not been as robust as years prior, revenue is still strong because rates increased so significantly during the boom of the COVID years.

The formula for the best performance is strong operations in strong markets. These are the facilities that earned the asset class its fame and popularity with investors. Generally speaking, in any economic conditions, most self-storage owners and investors would rather have self-storage than any other asset class.