his 2025 Capital Lender Survey offers a snapshot of lending sentiment within the self-storage sector, capturing insights from banks and credit unions actively engaged in commercial real estate finance. The results reflect perspectives from DXD partner institutions across the country, with responses collected from regional and community banks, national institutions, and credit unions. Participants provided their outlooks on lending strategies, portfolio concentration, underwriting criteria, and perceived risks within the current macroeconomic environment.

As the capital markets continue to evolve in response to high interest rates, shifting regulatory landscapes, and broader economic uncertainty, understanding lender behavior is more important than ever. This survey offers visibility into how capital providers are adjusting their self-storage loan strategies and where they may be pulling back or leaning in. What emerges is a picture of cautious consistency: Most lenders report steady appetite for self-storage yet remain sharply focused on managing risk through tighter underwriting and exposure controls.

As a consequence of the generous lending practices that occurred in 2021 and 2022, coupled with significant interest rate hikes leading to asset distress, banks have adopted a conservative lending approach today. This posture is expected to keep construction lending subdued for the next one to two years, thereby mitigating the risk of oversupply across numerous commercial real estate asset classes, particularly self-storage.

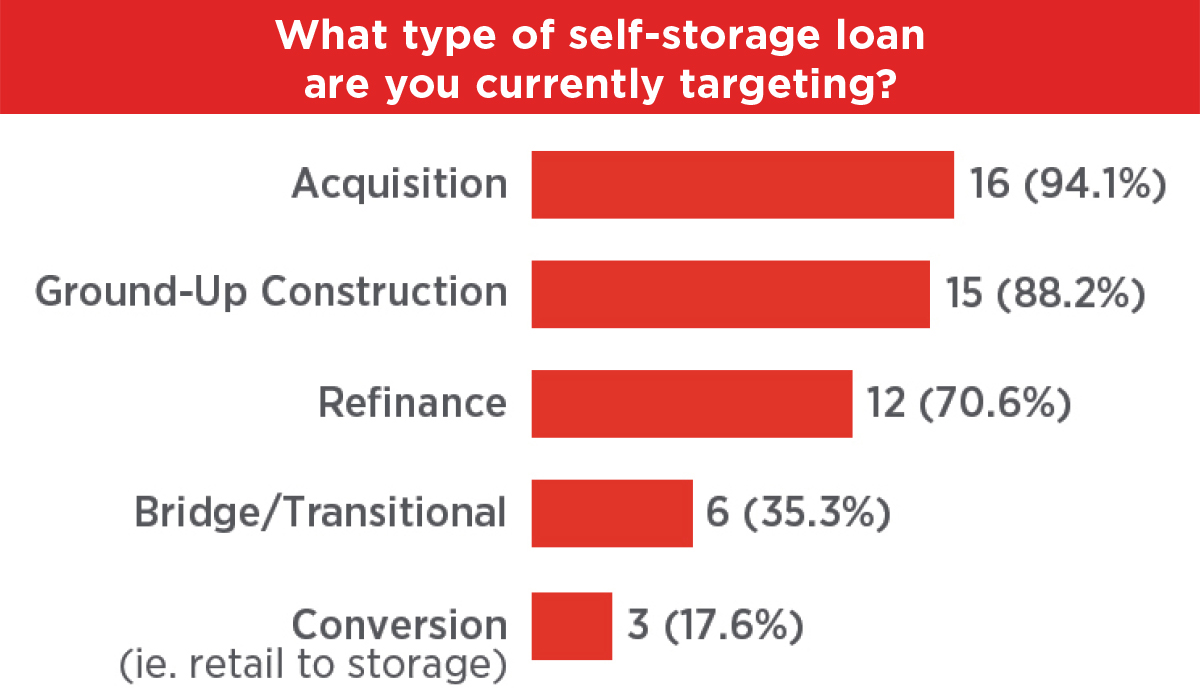

See Type Of Lending Institution chart and Type Of Loans chart.

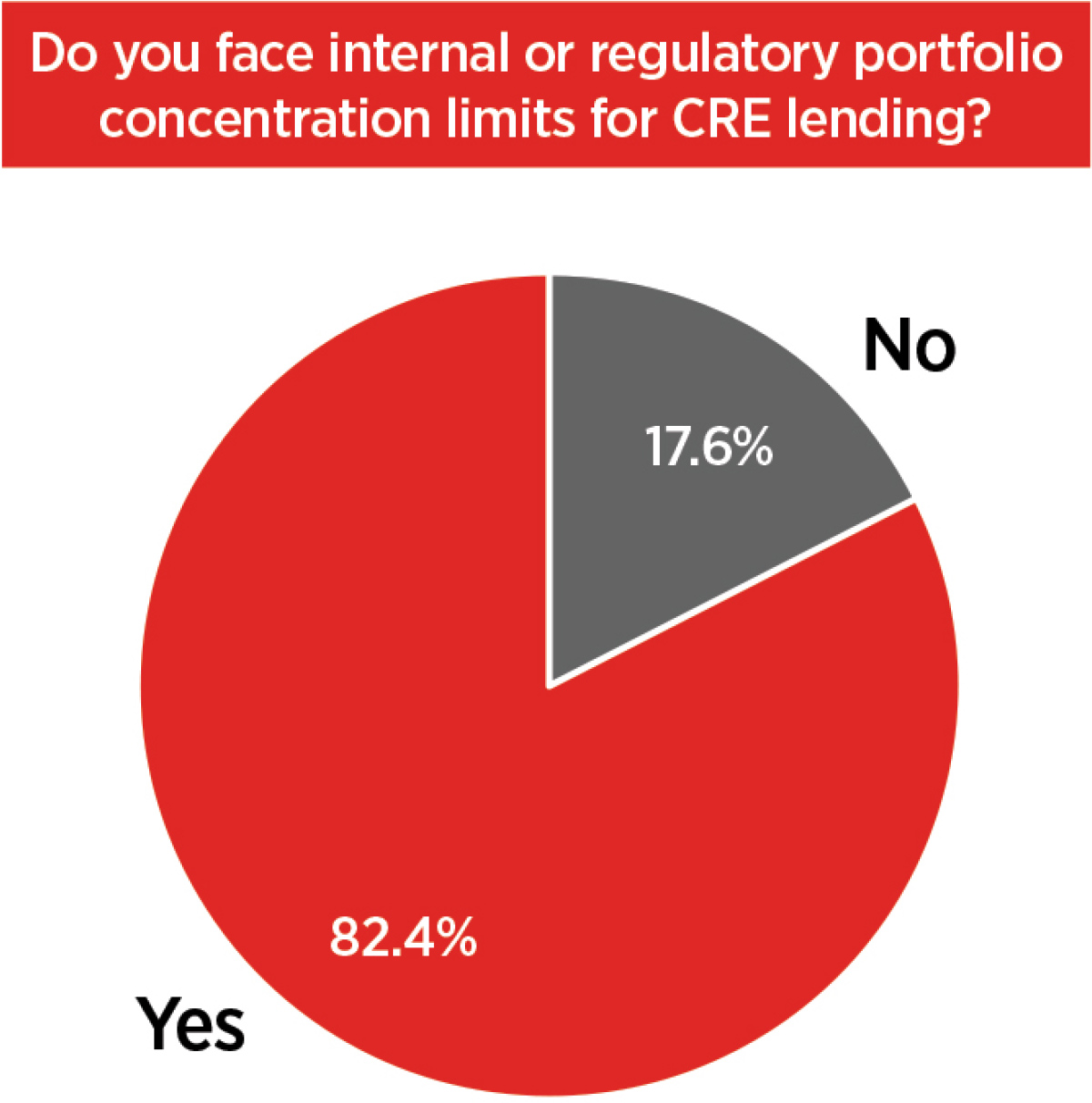

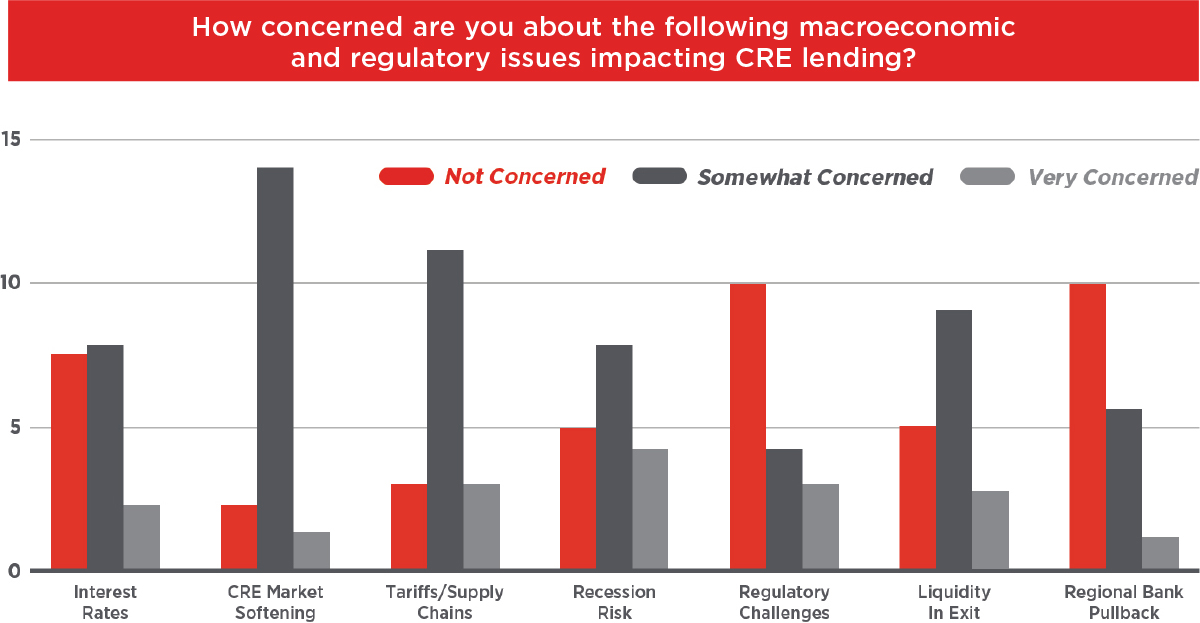

There is a measured but cautious stance among DXD lenders. Nearly half (47.1 percent) reported that self-storage loan performance was on par with other CRE sectors, while 23.5 percent noted underperformance and an equal share indicated a lack of sufficient data to evaluate. When ranking underwriting concerns, absorption risk during lease-up was the top issue (88.2 percent), followed by oversupply, sponsor capabilities, and construction costs. In terms of broader macroeconomic and regulatory pressures, lenders expressed the greatest concern over interest rates, CRE market softening, and recession risk, with regional bank pullback also registering as a key issue. Together, these insights underscore a lending environment shaped by risk mitigation and selectivity.

See Storage Performance CRE 12 Month chart, Concerned Macroeconomic and Regulatory Issues chart, and Top Three Underwriting Condcerns chart.

When ranking underwriting concerns, absorption risk during lease-up was the top issue (88.2 percent), followed by oversupply, sponsor capabilities, and construction costs. In terms of broader macroeconomic and regulatory pressures, lenders expressed the greatest concern over interest rates, CRE market softening, and recession risk, with regional bank pullback also registering as a key issue.

Together, these insights underscore a lending environment shaped by risk mitigation and selectivity.

Martin Huff

Managing Director – Investor Relations

(706) 615-2323 – martin@dxd.capital

Andrew Tuthill

Managing Director – Capital Formation

(415) 640-4099 – andrew@dxd.capital

The information contained in this 2025 CRE Lender Survey (Survey) is provided for informational purposes only and is not comprehensive. The Survey is based on third-party CRE lending institution’s responses to questions posed by DXD Capital (DXD). DXD makes no representations, warranties, or assurances, express or implied, regarding the accuracy, completeness, reliability, or suitability of the information provided in the Survey.

This Survey reflects the responding lenders’ perspectives, estimates, and expectations. It does not constitute DXD Capital’s opinions, commitments, recommendations, or assurances regarding future lending conditions, capital market dynamics, regulatory changes, or self-storage sector performance. Any reliance on the information in this Survey is at the sole risk of the recipient.

DXD expressly disclaims any liability for inaccuracies or incompleteness and for direct, indirect, or consequential losses arising from the use of or reliance on this Survey. The findings should not be construed as financial, legal, or professional advice. Readers are encouraged to conduct their own due diligence and consult with qualified professionals for specific guidance with respect to any business or investment decisions.