nvestment rates have declined slightly from Q1 2024, reflecting the common characteristics of self-storage: slow and steady over the long run. As Gary Sugarman, COO and principal of The William Warren Group, said, “Self-storage is great; it can’t always be unbelievable.”

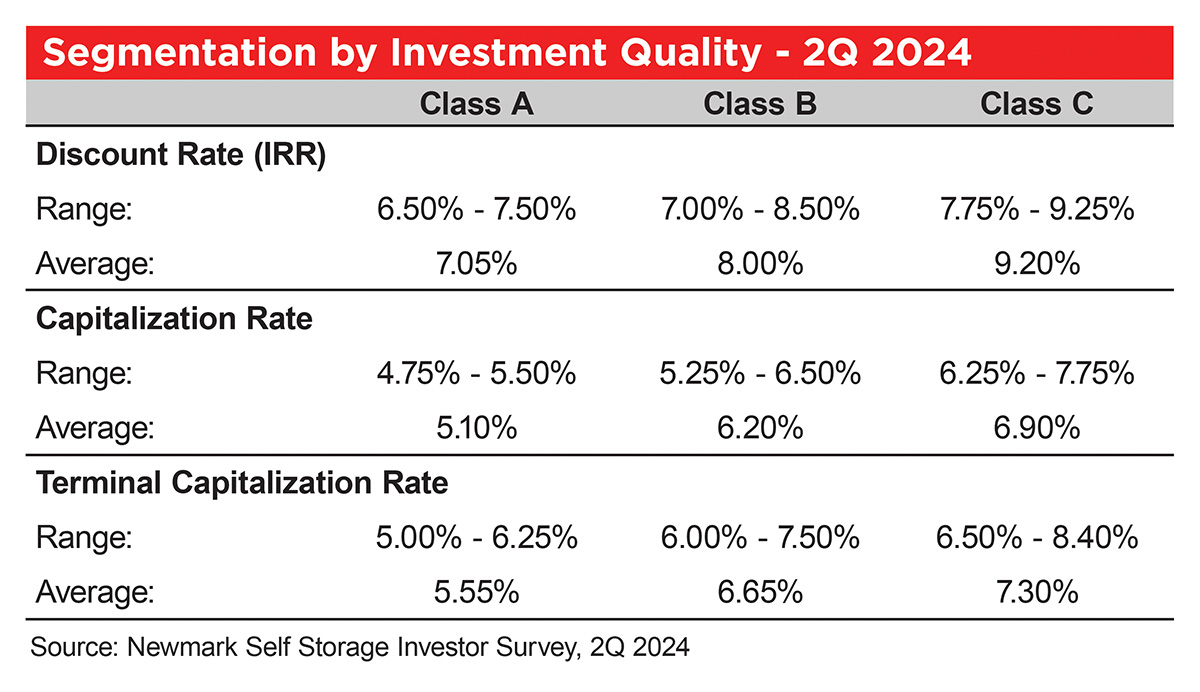

Cap rates declined slightly in the 2Q 2024 Investor Survey slightly, back to Q4 2023 levels approximately or a 7 bp decline from Q1 2024 levels to 5.76 percent. There is a near certain belief the Fed will cut rates in the near term, and that appears to be reflected in higher optimism this quarter. Key performance indicators are shown in the Segmentation by Investment Quality Table.

See Segmentation by Investment Quality Table

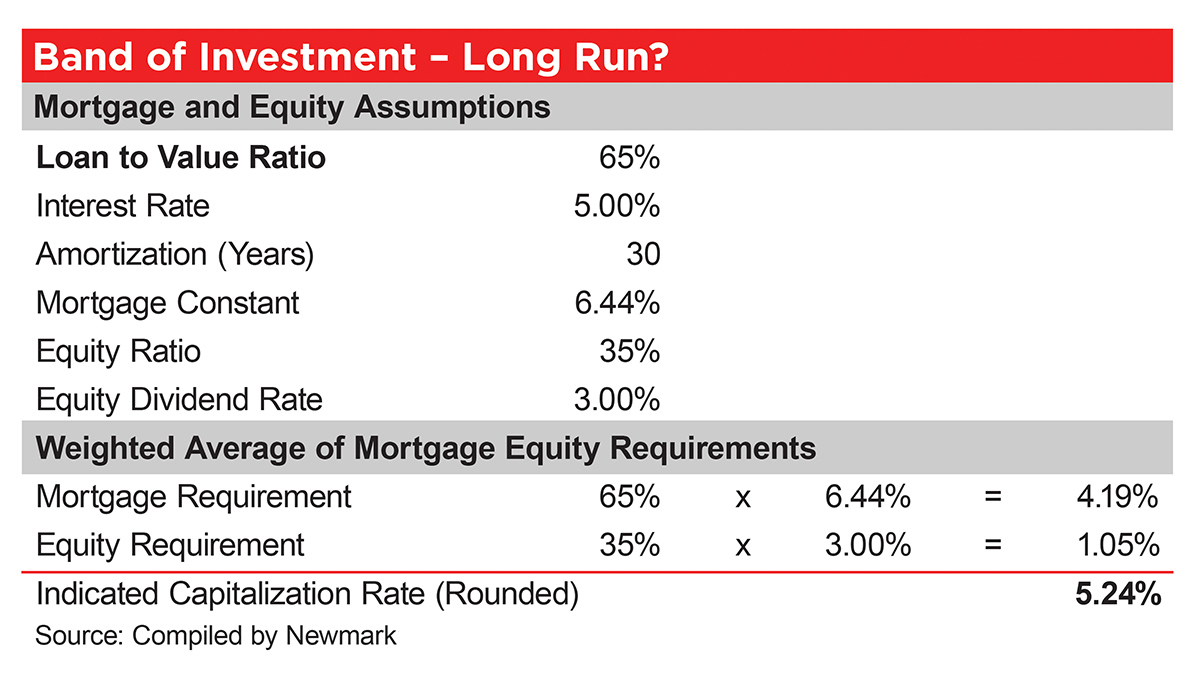

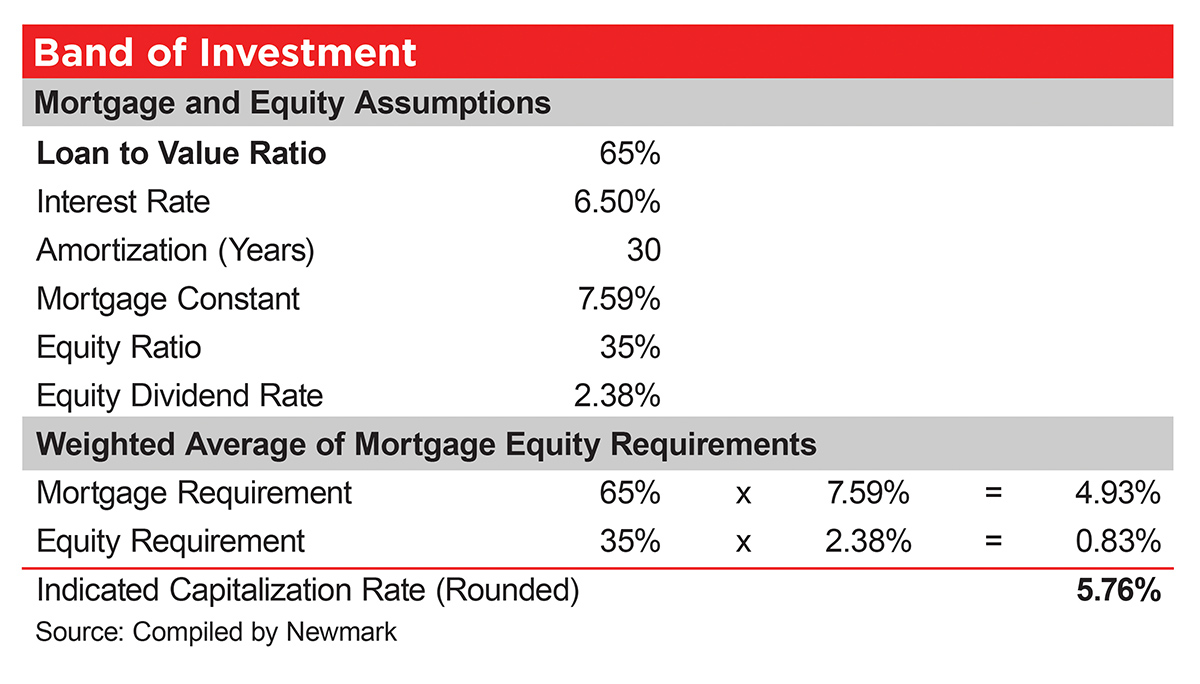

Absent knowledge (or my answer, I don’t know), let’s look at what math suggests. Solving for a current cap rate of 5.76 percent could look like the example in the Band of Investment Table.

See Band of Investment Table

See Band of Investment – Long Run Table