he self-storage industry has spent the better part of the last two years talking about a development slowdown. It makes sense when cost of construction is up, rates are down, and getting projects approved is harder than ever.

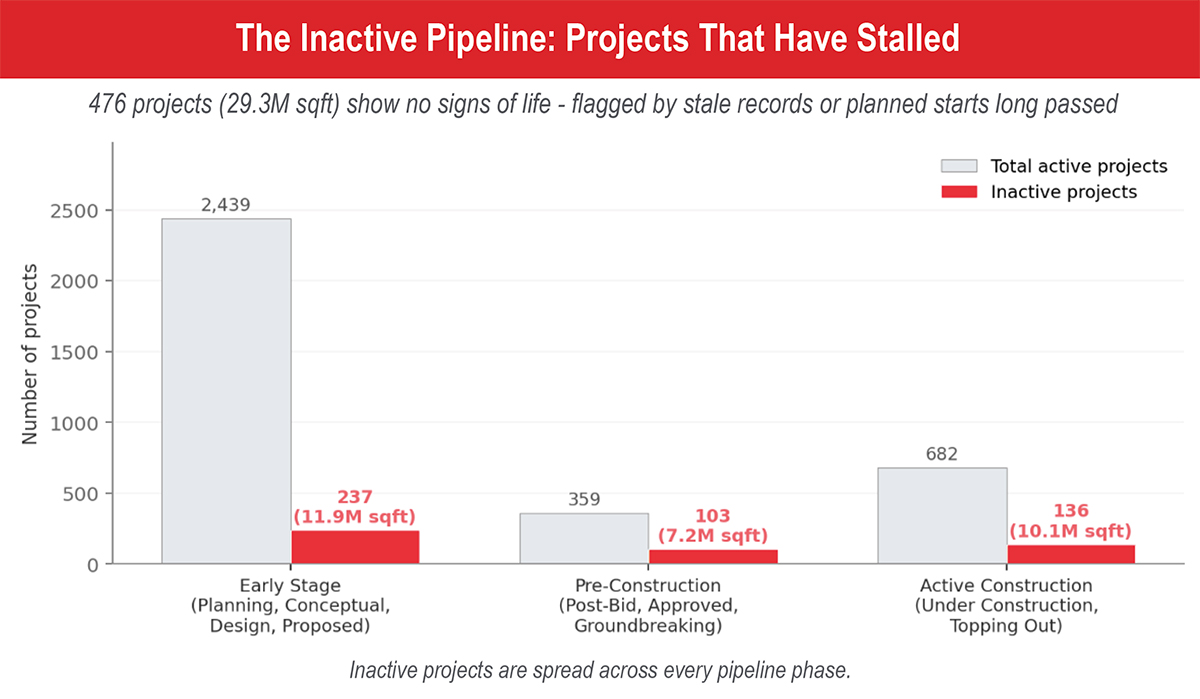

TractIQ currently tracks 395 self-storage projects with an official “Cancelled” status, representing roughly 23.1 million square feet of supply that was announced but never built. Sitting alongside that graveyard is a second larger population: 476 projects we’d call “inactive.” These projects are still listed as active in the pipeline yet show every sign of being abandoned.

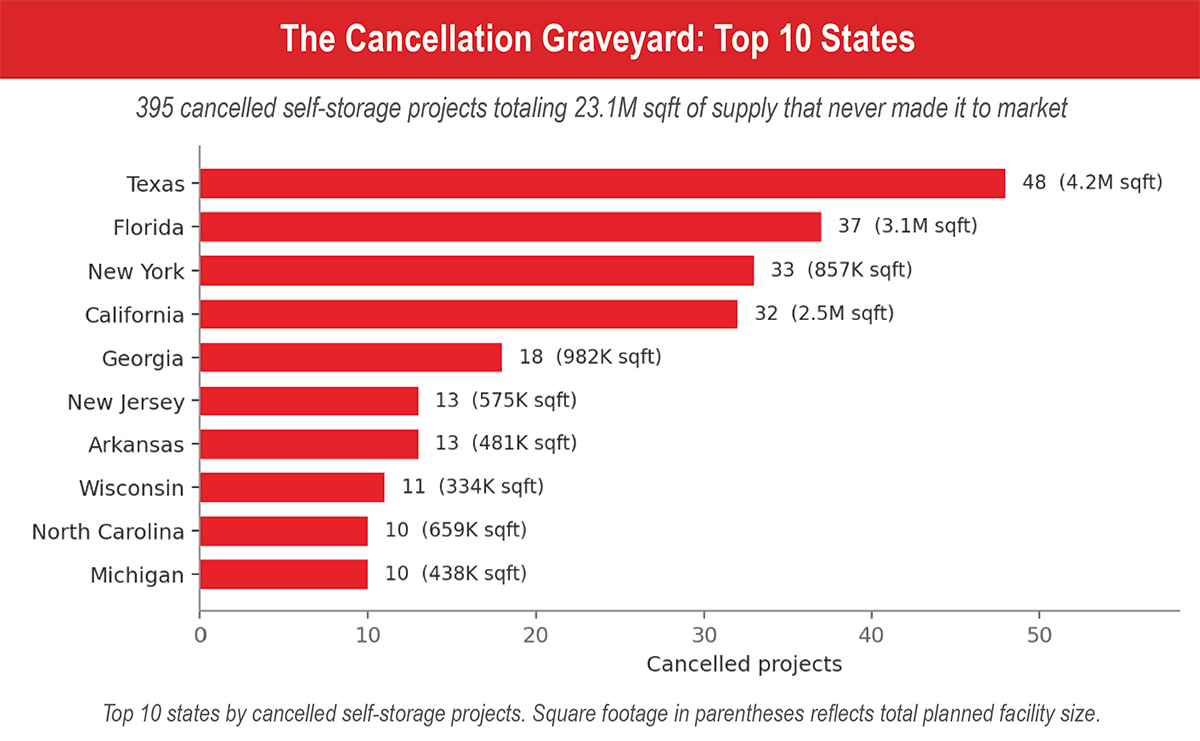

See The Cancellation Graveyard: Top 10 States chart.

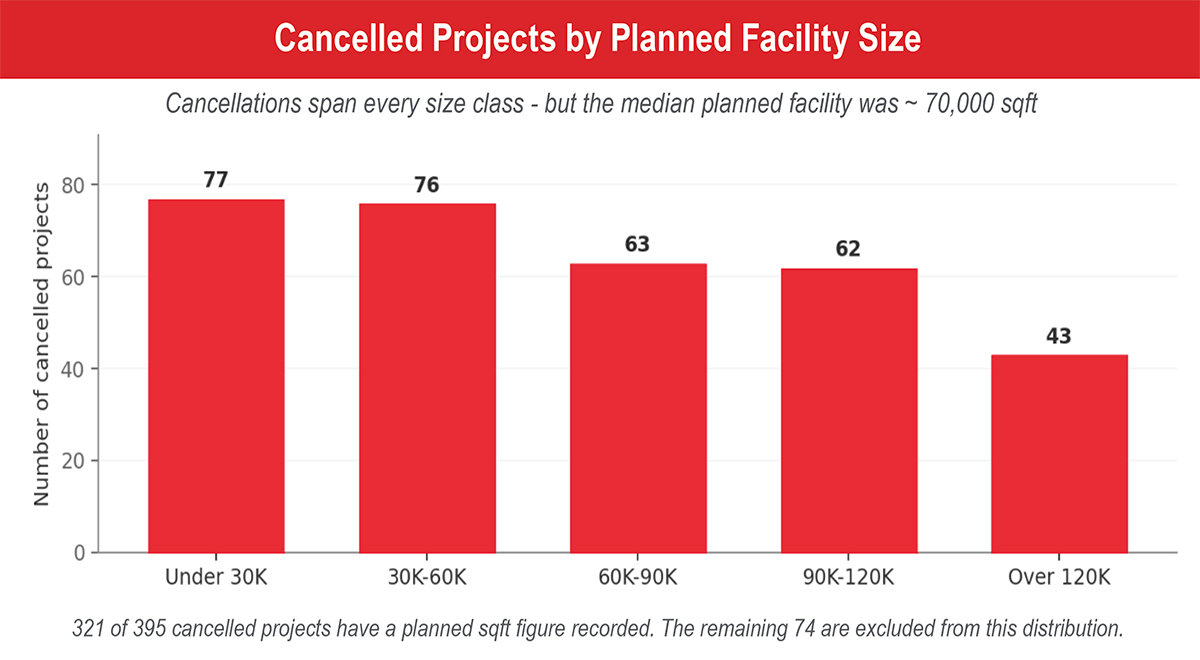

See Canceled Projects by Planned Facility Size chart.

If the cancellation graveyard captures projects that have formally been pulled, the inactive pipeline captures something messier: projects that are technically still in the pipeline but show no measurable signs of life. We flagged a project as inactive if either its TractIQ record hasn’t been touched in 18-plus months, or its planned start date passed more than a year ago without progression. By that definition, 476 active-pipeline projects qualify. This equals 29.3 million square feet, which is actually larger than the cancellation graveyard.

See The Inactive Pipeline: Projects That Have Stalled chart.

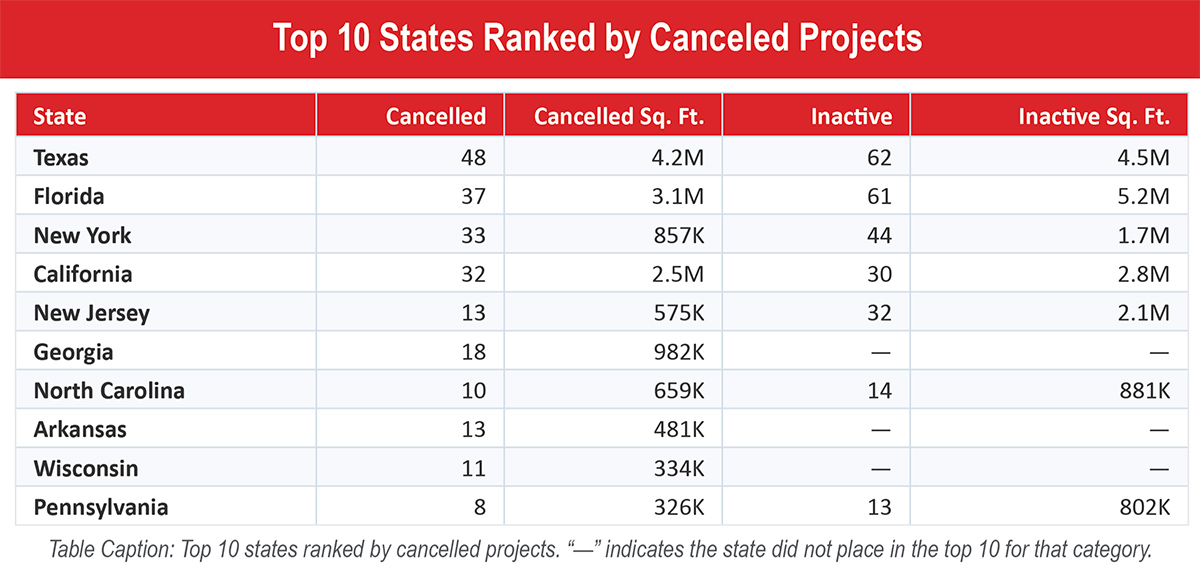

See Top 10 States Ranked by Canceled Projects table.

Data & methodology: All figures sourced from TractIQ’s self-storage pipeline database, queried May 2026. “Cancelled” projects are those explicitly marked with project status = “Cancelled.” “Inactive” projects are active-pipeline projects (excluding Cancelled) flagged by one of two signals: (1) record not updated in 18-plus months, or (2) a planned start date that has passed by more than 12 months.

Noah Starr is the CEO of TractIQ.