hroughout history, capital market cycles have been driven by the underlying forces of various economic dynamics, including local and national political policies. The beginning of the current market cycle can be defined as the start of President Trump’s term in office. He and his administration have been quick to take measures in reshaping the role and size of the government agencies, instituting ongoing tariffs with trade partners, signing an array of executive orders, and pushing for a budget that no doubt will have ramifications when it is eventually passed.

In most cycles, one can look back historically to disseminate similar characteristics to glean some guidance on potential consequences and outcomes. However, with swift and sometimes unpredictable executive orders and a changing federal and local political landscape, the ability to synthesize the effects specifically on the future cost becomes more difficult. We, however, can assess some market activity to date as a basis for what we may anticipate future interest rates may look like under the new administration. Let’s start by examining how both short-term variable rates and longer-term fixed rates are being impacted.

In January, the chairman of the Fed, Jerome Powell, gave guidance that we should expect to see two to three incremental decreases in 2025, and many economists had predicted as much as a 1.0 percent total decrease in rates. However, as of the May 2025 Fed meeting, Powell shifted to a “wait and see” approach, shying away from reference to additional rate decreases. He stated, “Uncertainty about the economic outlook has increased further,” and went on to affirm that, “costs of waiting to see further are fairly low, we think, so that’s what we’re doing.” The FOMC is in the tough position of trying to balance inflation with unemployment. The labor market and unemployment have shown strong signs of resilience, and inflation, although it has come down from pandemic highs, will likely be impacted by the eventual impact of tariffs, wherever they may land.

The federal funds rate is the most controllable factor that impacts interest rates because it is set simply by the decision of the FOMC. Any decision that the FOMC makes to notch down or up the Fed Funds Rate will have an impact on the cost of funds and self-storage business activity. For example, by decreasing the rate, variable rate loans will be lower, and a shovel-ready construction project may be closer to penciling out and moving forward, or a value-add purchase financed with a variable rate bridge may be more attainable.

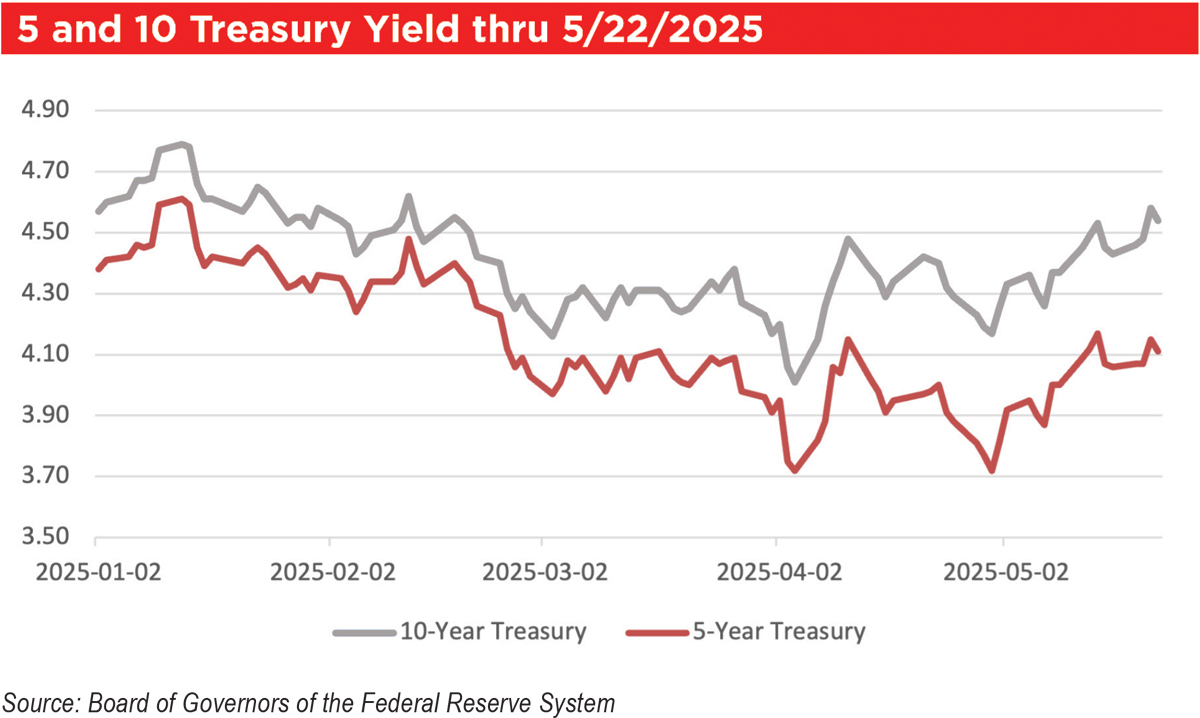

See 5 and 10 Treasury Yield chart.

Historically, Treasuries have tended to have at least a 1.0 percent range from low to high in a given year. Early signs are that the Treasury yields do show market fluctuations, but not in a remarkable difference from historic performance. Given the shock of swift changes, we can learn that the Treasury market is somewhat resilient. With some recent market activity, involving the beginning of a sell-off of Treasuries, we also learned that the market could react unfavorably if measures are pushed too far.

Although indices and spreads can both rise at the same time, most of the increases in spread happened at the same time indices were dropping, and vice versa. Many times, the offset effect is not equal but lessens net volatility.

The current overall mortgage rates range varies based on each transaction. The lowest financing terms are in the mid- to high-5 percent range for low risk/institutional properties and investors, while most loans fall into the 6.0 percent to 7.0 percent range, and lower quality, lower debt service coverage, and higher leverage loans may be priced with rates of 7.0 percent and above. Except for an extraordinary low interest rate environment that we enjoyed from 2008 to 2023, the current rates are well within the historic rates going back before the great financial crisis.

This all appears to be leading to a trend of behavior by many to leaning to less risky, safer decisions. We are seeing that play out in the pricing of debt. The loan requests that have less risk are seeing spreads tighten. Conversely, for transactions or financing of lower quality and higher leverage transactions that are generally less attractive, lenders are often cutting proceeds or widening spreads.

Each market cycle will have unique circumstances, causing a new set of criteria to consider when seeking financing. Today, the loan quotes are likely to look quite different from one to another, and lenders will all have slightly different directives, all trying to make sound business decisions based on how they are interpreting the market.

Despite market uncertainty, much of which is self-imposed by the current President, the underlying indices have moved within their fairly tight ranges, and most importantly, the capital providers widely remained open for business and to lending. Interest rates and terms will vary, sometimes widely, based on the loan request and which institutions are providing loan terms.

The leadership under this administration believes they have a mandate and will continue to reshape the nation one day at a time. So far, just isolating the impact on capital availability and rates, there has been volatility but not drastic shifts.